Introduction

Vertical mergers are once again a hot topic. Over the past several years, commentators have vigorously debated whether the approach traditionally taken by the US Federal Trade Commission (“FTC”) and US Department of Justice Antitrust Division (“DOJ”) (collectively, the “Agencies”) is fully aligned with economic thinking that is both au courant and administrable. Recently, talk has turned to action: in the past three years, DOJ litigated the first agency-led vertical merger challenge in approximately forty years,1See United States v. AT&T Inc., 310 F. Supp. 3d 161, 193–94 (D.D.C. 2018), aff’d, 916 F.3d 1029 (D.C. Cir. 2019). the Agencies held the first public hearings on vertical mergers in many years,2See FTC Hearing #5: Vertical Merger Analysis and the Role of the Consumer Welfare Standard in U.S. Antitrust Law, Fed. Trade Commission (Nov. 1, 2018), https://perma.cc/P7SW-3LWD; Public Workshops on Draft Vertical Merger Guidelines, U.S. Dep’t of Justice, Antitrust Div. (June 26, 2020), https://perma.cc/2KV9-2TE3. and the Agencies issued new Vertical Merger Guidelines, the first jointly issued agency guidance on the topic.3U.S. Dep’t of Justice & Fed. Trade Comm’n, Vertical Merger Guidelines (2020), https://perma.cc/389K-H8FP.

In these discussions, some argue that vertical mergers pose at least the same anticompetitive potential as their horizontal brethren, and therefore deserve equal skepticism and scrutiny.4See, e.g., Jonathan B. Baker, Nancy L. Rose, Steven C. Salop & Fiona Scott Morton, Five Principles for Vertical Merger Enforcement Policy, 33 Antitrust 12, 14 (2019) (“[E]nforcers also should not set a higher evidentiary standard for finding anticompetitive harms from a vertical merger than it applies when reviewing horizontal deals.”) Yet, this view is at odds with most of the economic literature, which generally finds that vertical mergers (and restraints) generate greater procompetitive benefits than horizontal mergers, typically making them, on net, procompetitive. First and foremost, vertical mergers allow the merged firm to eliminate a markup it would otherwise pay a supplier; this dynamic is called the elimination of double marginalization (“EDM”). Whereas EDM is an inherent or unilateral effect, vertical mergers also produce a number of standard efficiencies, like more efficiently allocating risk and incentivizing asset-specific investments, which benefit consumers by expanding output.

This is not to say that all vertical mergers and restraints are lawful. Vertical mergers may also allow a firm to engage in anticompetitive conduct, like raising rivals’ costs (“RRC”), complete foreclosure, or misuse of information. Yet RRC and EDM are both inherent, unilateral competitive effects—two sides of the same coin—even if they do not necessarily share equal magnitude. As a result, the economic literature finds that a vertical merger’s aggregate procompetitive benefits are likely to exceed its anticompetitive effects across a wide range of—but not all—possible scenarios.5See, e.g., D. Bruce Hoffman, Acting Dir., Bureau of Competition, Fed. Trade Comm’n, Remarks on Vertical Merger Enforcement at the FTC at Credit Suisse 2018 Washington Perspectives Conference 4 (Jan. 10, 2018), https://perma.cc/W9TW-R5F6 (“To summarize, overall there is a broad consensus in competition policy and economic theory that the majority of vertical mergers are beneficial because they reduce costs and increase the intensity of interbrand competition. That consensus has support in the empirical research. Does that mean all vertical mergers are benign? No, it doesn’t.”).

Yet the law has not always followed the economics, and sometimes has explicitly parted ways with it. In the mid-twentieth century, the law viewed efficiencies as either irrelevant or anticompetitive, and it therefore condemned many vertical mergers.6See infra Section II.A. Of course, this was the same era when comprehensive sectoral regulation was celebrated despite its destructive consequences for consumers, the originally intended beneficiaries of these byzantine legal frameworks.7See, e.g., Christine S. Wilson & Keith Klovers, The Growing Nostalgia for Past Regulatory Misadventures and the Risk of Repeating These Mistakes with Big Tech, 8 J. Antitrust Enf’t 10, 12–14 (2019) (recounting the genesis and early history of the Interstate Commerce Commission and Civil Aeronautics Board).

Ultimately the tide shifted with economic analysis leading the way.8See, e.g., Oliver E. Williamson, Markets and Hierarchies: Analysis and Antitrust Implications (1975); Roger D. Blair & David L. Kaserman, A Note on Bilateral Monopoly and Formula Price Contracts, 77 Am. Econ. Rev. 460 (1987); Paul L. Joskow, The Role of Transaction Cost Economics in Antitrust and Public Utility Regulatory Policies, 7 J.L. Econ. & Org. 53 (1991); Benjamin Klein, Robert G. Crawford & Armen A. Alchian, Vertical Integration, Appropriable Rents, and the Competitive Contracting Process, 21 J.L. & Econ. 297 (1978). Year by year, the economic evidence has indicated ever more clearly that vertical integration—whether by merger or otherwise—is typically procompetitive.9See infra Part I; see also Roger D. Blair & D. Daniel Sokol, The Rule of Reason and the Goals of Antitrust: An Economic Approach, 78 Antitrust L.J. 471, 491 n.90 (2012) (noting that vertical integration through merger can lead to “increased competition”); Leah Brannon & Douglas H. Ginsburg, Antitrust Decisions of the U.S. Supreme Court, 1967 to 2007, 3 Competition Pol’y Int’l 3, 12 (2007) (same); William E. Kovacic & Carl Shapiro, Antitrust Policy: A Century of Economic and Legal Thinking, 14 J. Econ. Persp. 43, 53 (2000) (same); D. Daniel Sokol, The Transformation of Vertical Restraints: Per Se Illegality, the Rule of Reason, and Per Se Legality, 79 Antitrust L.J. 1003, 1006 (2014) (same). The shift towards economically informed legal analysis profoundly affected the design of sector regulations, from transportation, to banking, to energy. As a result, most sectoral regulations banning vertical integration have fallen,10See Wilson & Klovers, supra note 7, at 10–12. as have other vertical restraints harmful to consumer welfare.11See Sam Peltzman & Clifford Winston, Deregulation of Network Industries (2000) (describing the deregulation of various industries); Paul L. Joskow & Nancy L. Rose, The Effects of Economic Regulation, in 2 Handbook of Industrial Organization 1485 (Richard Schmalensee & Robert Willig eds., 1989) (explaining how the deregulation of the airline industry since 1978 has improved consumer welfare); Paul L. Joskow, Regulation and Deregulation After 25 Years: Lessons Learned for Research in Industrial Organization, 26 Rev. Indus. Org. 169, 169–70, 188–89 (2005) (outlining the deregulation in various industries that began in the 1970s).

The recognition that vertical integration is typically procompetitive also required a significant course correction in antitrust law and policy. In the late 1970s, vertical mergers became more difficult to challenge.12See infra Part II. In 1984, the DOJ revised its Merger Guidelines to recognize that vertical mergers “are less likely than horizontal mergers to create competitive problems.”13U.S. Dep’t of Justice, Merger Guidelines 23 (1984), https://perma.cc/7WQF-ALW8. As a result, the Agencies and the parties resolved almost all vertical merger concerns via consent agreements (“consents”),14See Steven C. Salop & Daniel P. Culley, Revising the US Vertical Merger Guidelines: Policy Issues and an Interim Guide for Practitioners, 4 J. Antitrust Enf’t 1, 25 & n.80, 28 & n.92 (2015). Some consents may have been less effective. See Steven C. Salop, Invigorating Vertical Merger Enforcement, 127 Yale L.J. 1962, 1976, 1992 (2018). Antitrust agencies should take care to craft effective consents. For remedying some of the limitations of existing consents, see, for example, Press Release, U.S. Dep’t of Justice, Antitrust Div., Justice Department Will Move to Significantly Modify and Extend Consent Decree with Live Nation/Ticketmaster (Dec. 19, 2019), https://perma.cc/JB8P-GE2N; Press Release, Fed. Trade Comm’n, FTC Imposes Conditions on UnitedHealth Group’s Proposed Acquisition of DaVita Medical Group (June 19, 2019), https://perma.cc/DFJ5-DXRX; Press Release, Fed. Trade Comm’n, FTC Imposes Conditions on Northrop Grumman’s Acquisition of Solid Rocket Motor Supplier Orbital ATK, Inc. (June 5, 2018), https://perma.cc/CE8G-TKAJ. which ranged from the traditional to the quixotic,15See, e.g., Christine S. Wilson & Keith Klovers, Yes We Can, But Should We?: Merger Remedies During the First Obama Administration, Competition Pol’y Int’l Antitrust Chronicle 2 (Dec. 2014). and in the handful of remaining cases, the parties abandoned the merger. Indeed, it took almost forty years for the Agencies to litigate another vertical merger challenge, United States v. AT&T Inc.,16310 F. Supp. 3d 161 (D.D.C. 2018). and to issue new Vertical Merger Guidelines. The Vertical Merger Guidelines acknowledge that “the agencies more often encounter problematic horizontal mergers than problematic vertical mergers”17Dep’t of Justice & Fed. Trade Comm’n, supra note 3, at 2. and describe an approach in which the Agencies will balance the tradeoff of procompetitive effects of EDM with the harms resulting from RRC. We call this the “unilateral effects tradeoff.”18Id. at 4–5 (describing how the Agencies will evaluate the “net effect” of EDM and RRC).

Given this economic and legal history, the best way for antitrust law and policy to distinguish potentially anticompetitive vertical mergers from potentially procompetitive or competitively benign ones is not, as some populists have argued, to simply ban all such mergers.19For example, Professor Lina Khan argues that “[t]he best way to preserve fair and open competition is . . . simply to completely ban any network monopolist from owning businesses that place it in competition with the companies that depend on it to reach [the] market . . . [which] is what previous generations did with railways.” Kevin Carty, Leah Douglas, Lina Khan & Matt Stoller, 6 Ideas to Rein in Silicon Valley, Open Up the Internet, and Make Tech Work for Everyone, N.Y. Mag.: Intelligencer (Dec. 11, 2017), https://perma.cc/XZ94-FS5H. Rather, following the approach set out by the D.C. Circuit in AT&T, policymakers should create a series of presumptions, based on economic effects and a careful case-by-case analysis using existing empirical tools (and recalibrating those tools over time as economic learning advances)20James Bernard, Rebecca Kirk Fair & D. Daniel Sokol, Why Does the Consumer Welfare Standard Work? Matching Methods to Markets, Competition Pol’y Int’l Antitrust Chron., Nov. 2019, at 1–7. to assess the likely economic effects of a given vertical merger. Although “the lack of rules or even presumptions on vertical mergers” is untenable,21Open Markets Institute, American Economic Liberties Project, Frank Pasquale & Maurice Stucke, Comment Letter on Draft Vertical Merger Guidelines, at 16 (Feb. 10, 2020), https://perma.cc/CHC9-QWAE. it makes little sense to reflexively “readopt”22See id. at 1, 21–24 (urging readoption of the Department of Justice’s 1968 Merger Guidelines). bygone legal rules that were then, and even more surely are now, divorced from economic learning.

Rather, policymakers should adopt and refine the burden-shifting framework set out in United States v. Baker Hughes, Inc. 23908 F.2d 981, 991–92 (D.C. Cir. 1990). and first applied to vertical mergers in AT&T.24United States v. AT&T, Inc., 310 F. Supp. 3d 161, 191 (D.D.C. 2018). Although this approach is generally accepted, the discussion today on burden shifting misses two critical refinements. First, because EDM and RRC are two sides of the same coin, if a plaintiff alleges an RRC theory of harm, then it should bear the burden (in step one) of demonstrating that the merger is likely to produce a net unilateral anticompetitive effect. Such an approach is consistent with the Vertical Merger Guidelines, which state that the Agencies will assess the “net effect” of all changes to a merged firm’s unilateral incentives.25Dep’t of Justice & Fed. Trade Comm’n, supra note 3, at 5. In litigation, this goal is achieved only if the analysis addresses both RRC and EDM; specifically, the plaintiff must show that the anticompetitive effect of RRC likely exceeds the procompetitive benefit of EDM in the instant case—the unilateral effects tradeoff. The same logic also likely applies to complete foreclosure, which is simply a more extreme form of RRC. This approach should guide both judicial review and agency enforcement.

Second, if the plaintiff carries its burden at step one, then the defendant should be able to argue, and courts and Agencies should seriously consider, the full range of procompetitive efficiencies. As economists have long known, vertical integration can expand output by reducing transaction costs, better allocating risk, diffusing new technologies and techniques, reducing inventory costs, and better coordinating investment decisions. These efficiencies are real and should be credited when proven. Given the state of the literature on the efficacy of vertical contracting and the approach used in horizontal mergers, defendants in these cases should not bear the burden of demonstrating that every hypothetical alternative method of achieving these efficiencies is closed to them. That is, antitrust needs to embrace a “holistic efficiency analysis,” which incorporates this broader set of efficiencies that is well recognized in the academic literature.

This Article is structured in three parts. Part I examines the economic literature, both theoretic and empirical. Part II reviews the legal history, starting with passage of the Clayton Act in 1914. Part III sets out the proposed legal framework that synthesizes the economics and the law.

I. Economics of Vertical Mergers and Vertical Restraints

Vertical integration refers to a firm’s decision to operate at two (or more) stages in the production and distribution of a product. For example, suppose that a downstream retail grocery chain owned an upstream dairy farm that produced raw milk,26In discussing the distribution chain from the initial production stage to the final consumer, “downstream” refers to the move of goods towards the final consumer. Thus, when raw milk moves from a dairy farm to a milk processor, it is moving downstream. Movements “upstream” are the opposite, that is, these movements are further away from the final consumer. which it transferred to its retail outlets after processing. The chain would be vertically integrated from the production stage to the processing stage to the retail distribution stage.

A merger integrating two firms along the same vertical chain incentivizes each formerly separate firm to account for the effect of its actions on its merging partner. For example, an unintegrated retailer’s profits may increase if a wholesaler decreases its price to that retailer. The same retailer’s profits may also increase if the wholesaler raises its price to the retailer’s competitors. Finally, the retailer’s price may affect the profit earned by the wholesaler via sales to other retailers, as consumers substitute across retailers based on price. Unintegrated firms ignore the effect of their actions on the profits of other firms; integrated firms optimally internalize how their actions affect their upstream and downstream affiliates.

Horizontal merger enforcement is commonly premised on a single analogous change to a unilateral incentive.27Coordinated theories of harm also exist for horizontal mergers. See, e.g., Nathan H. Miller & Matthew C. Weinberg, Understanding the Price Effects of the MillerCoors Joint Venture, 85 Econometrica 1763, 1788–89 (2017). However, the focus in merger enforcement since the 1992 Horizontal Merger Guidelines has been on unilateral effects. A firm can increase the profit of any other horizontally related firm by raising its price, thus diverting some of its demand to that firm. Unintegrated firms ignore this external effect, while integrated firms internalize the effect by increasing price to the detriment of consumers. Antitrust scrutiny of horizontal mergers often proceeds by measuring the effect of the unilateral incentive to increase price against that of productive efficiencies generated by the merger.

In contrast, vertical mergers generate a more complex set of unilateral incentives, some of which typically benefit consumers and some of which typically harm consumers. The net effect of these incentives is ambiguous as a theoretical matter, meaning vertical mergers often benefit consumers even in the absence of productive efficiencies. Accounting for both unilateral incentives and productive efficiencies, the empirical literature finds that vertical mergers usually benefit consumers. For example, Professors Francine Lafontaine and Margaret Slade survey the empirical literature and find that it “is highly supportive of the efficiency of vertical integration and mergers . . . [and] indicates that integration benefits consumers.”28Francine Lafontaine & Margaret Slade, Vertical Integration and Firm Boundaries: The Evidence, 45 J. Econ. Lit. 629, 675 (2007). Two other surveys find similarly strong evidence that vertical integration generally benefits consumers.29James C. Cooper, Luke M. Froeb, Dan O’Brien & Michael G. Vita, Vertical Antitrust Policy As a Problem of Inference, 23 Int’l J. Indus. Org. 639, 658 (2005) (“Most studies find evidence that vertical restraints/vertical integration are procompetitive . . . .”); Global Antitrust Institute, Comment Letter on the Federal Trade Commission’s Hearings on Competition and Consumer Protection in the 21st Century, at 6–7 (Sept. 6, 2018), https://perma.cc/SDG2-PM3A (finding that, of eleven papers written since 2008 identifying welfare implications of vertical integration, six found “positive welfare changes; four [found] no change, a mixed change, or no economically meaningful change . . . and only one (and perhaps two) had results that are consistent with a negative impact”). But see Marissa Beck & Fiona Scott Morton, Evaluating the Evidence on Vertical Mergers (Feb. 26, 2020) (unpublished comment), https://perma.cc/GVZ6-X8NY (cautioning against strong inferences drawn from the vertical merger retrospectives surveyed by Lafontaine & Slade, Cooper et al., and the Global Antitrust Institute). In United States v. AT&T, Inc., the district court was persuaded by evidence that three similar past vertical mergers did not result in price increases.30See United States v. AT&T, Inc., 310 F. Supp. 3d 161, 215 (D.D.C. 2018).

Determining prospectively whether a particular merger is likely to harm or benefit consumers necessarily involves a weighing of procompetitive and anticompetitive unilateral effects, even before accounting for productive efficiencies. Horizontal mergers have widely accepted indicia for likely unilateral harm.31See, e.g., U.S. Dep’t of Justice & Fed. Trade Comm’n, Horizontal Merger Guidelines 20 (2010) [hereinafter Horizontal Merger Guidelines], https://perma.cc/Q9HL-WNPV (“Unilateral price effects are greater, the more the buyers of products sold by one merging firm consider products sold by the other merging firm to be their next [best] choice.”). No such indicia exist for vertical mergers. Evidence that anticompetitive effects are likely to be large is unavailing if it is not analyzed concurrently with procompetitive effects.32See Gopal Das Varma & Martino De Stefano, Equilibrium Analysis of Vertical Mergers, 65 Antitrust Bull. (forthcoming 2020) (manuscript at 2–3), https://perma.cc/DHA9-WE8J (“[W]e show that RRC and EDM are not two separate effects. Instead, they are inseparably linked because the extent of EDM affects the strength of the RRC incentive, making EDM to be not just a stand-alone competitive benefit to be weighed against RRC.”). Thus, while neither economic theory nor empirical evidence rule out the possibility of harmful vertical mergers, both suggest that such mergers may be difficult to distinguish from more common procompetitive vertical mergers, outside of special circumstances.33See infra Section I.C.3.

The remainder of this Section describes procompetitive effects (including productive efficiencies) and anticompetitive effects of vertical mergers in greater detail. It then discusses balancing the two effects and the types of evidence that might support an inference of harm.

A. Procompetitive Effects of Vertical Integration

This Section discusses both a procompetitive unilateral effect—the elimination of double marginalization—and procompetitive efficiencies. EDM is an inherent result of a vertical merger that must be analyzed concurrently with any anticompetitive unilateral effects. Some of the efficiencies that may result from vertical mergers have close analogues to those commonly resulting from horizontal mergers, while others may be unique to vertical merger analysis. The breadth and likelihood of productive efficiencies that may result from vertical mergers demands that efficiencies be given serious attention before reaching a conclusion that a vertical merger is likely to harm consumers. This Section addresses primarily the circumstance in which vertical integration is achieved by merger.

1. Elimination of Double Marginalization

The literature on EDM traces back to Professor Joseph J. Spengler, who recognized that upstream and downstream monopolists, operating independently, price inefficiently because they choose their own markups without reference to one another.34See Joseph J. Spengler, Vertical Integration and Antitrust Policy, 58 J. Pol. Econ. 347, 349 (1950). When an upstream firm sells its output, it will maximize profits by setting price above its marginal cost, weighing the benefit of a higher margin against the reduction in demand caused by a higher price. A downstream firm treats the upstream firm’s price as part of its cost and imposes its own markup when it sells its own output, for the same reason the upstream firm charges a markup. In effect, there is a markup on a markup.

A vertical merger incentivizes the combined firm to eliminate the double markup. Before merging, when the upstream firm sets its price, it ignores that a decrease in its price raises the downstream firm’s profit and instead maximizes only its own profit. After merging, the combined firm internalizes the effect of the upstream price on downstream profit and thus lowers the upstream price.

Indeed, the integrated firm optimally will lower the upstream markup charged to the integrated downstream firm all the way to zero. Any internal transfer price paid from the downstream firm to the upstream firm neither increases nor decreases the combined firm’s overall profit. Instead, the transfer price lowers the profit of the downstream firm but increases the profit of the upstream firm by the same magnitude. Hence, the upstream firm optimally sets its internal price to the downstream firm to reflect the overall cost of the input to the firm.35External factors, such as the tax code, may affect these transfer prices.

Because it considers the impact of its choices on its affiliate, the merged firm earns a profit greater than the sum of the upstream and downstream profits of the unintegrated firms. This merger also benefits consumers: as the final good price falls, quantity rises, and both consumer welfare and total welfare increase. These results can be illustrated with a relatively simple economic model.

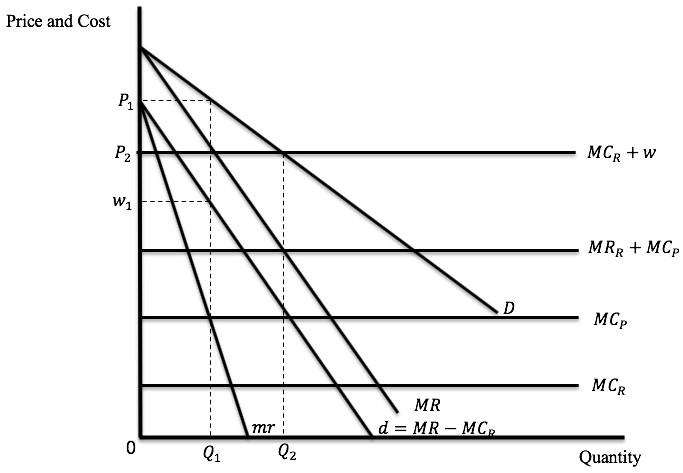

Figure 1

Suppose an upstream wholesale monopolist manufactures a product while an independently owned and operated downstream retail monopolist sells the product at retail.36EDM is illustrated using successive monopolists to abstract away from other unilateral effects that would result from a vertical merger of oligopolists. Our EDM analysis would extend to this case unaltered. In Figure 1, D represents the demand for the final product as sold by the retailer and MR is the associated marginal revenue. The marginal cost of performing the retail function is MCR.

The retailer maximizes its profit by setting marginal revenue equal to marginal cost. For the retailer, its marginal cost is the sum of the marginal cost of retailing (“MCR”) and the wholesale price that the retailer pays to the wholesaler. Thus, profit maximization requires purchasing and selling that quantity where MR = MCR + w1. Rearranging the condition provides the wholesaler’s derived demand: w1 = MR – MCR, which is labeled d = MR – MCR in Figure 1. As one can see, d is parallel to MR; the vertical distance between MR and d is the marginal cost of retailing, MCR. The corresponding marginal revenue of d is mr.

The wholesaler optimally will produce where its marginal revenue (“MR”) is equal to its marginal cost of production (“MCP”). The wholesale price (“w1”) is found on the derived demand d at the profit-maximizing quantity, which is Q1. Thus, the wholesaler produces Q1 and sells it to the retailer at a price of w1. Its profit is equal to (w1 – MCP)Q1.

The retailer will maximize its profit by buying and reselling that quantity where its marginal revenue (“MR”) is equal to its marginal cost, which is w1 + MCR. As one can see in the figure, the profit maximizing quantity is Q1 and the corresponding price is P1. The retailer’s profit is (P1 – w1 – MCR)Q1.

As both the wholesaler and retailer set a price above marginal cost, there is double marginalization. Were the wholesaler and retailer to vertically integrate, the combined firm would maximize its profit by equating the marginal revenue (“MR”) on sales of the final good to its total marginal cost of production and retailing (MCP + MCR). The profit maximizing quantity is Q2 and the corresponding price is P2. Thus, integration causes the retail price to fall from P1 to P2 and the quantity sold increases from Q1 to Q2. Under vertical integration, the combined firm sets a single markup over its combined cost of production and retailing, MCP + MCR.

EDM results when the merged firm internalizes the negative pricing externality that its upstream price has on its downstream margin; therefore, EDM is likely to result from any vertical merger for which this type of externality exists. Consequently, this phenomenon will arise in any vertical merger in which the downstream firm is a current customer of the upstream firm and pays a markup over the upstream firm’s costs. It will also arise in vertical mergers involving a downstream firm that does not currently purchase from the upstream firm but would likely do so after integration. Indeed, EDM may even arise in vertical mergers in which the downstream firm is unlikely to purchase from the upstream firm after integration, if the merger would improve the bargaining position of the downstream firm when negotiating with its unintegrated supplier.

Although EDM is a common phenomenon in vertical mergers, it is not always present. For example, EDM may not occur if the upstream firm’s product is technologically incompatible with the downstream firm’s needs. Similarly, if an already vertically integrated firm acquires an upstream rival, there may be no double margin to eliminate. Finally, if unintegrated firms have been able to completely eliminate double margins via contract, then their merger would, by definition, not result in EDM (although the mere possibility of achieving EDM via contract should not meaningfully alter analysis of EDM in any particular merger37See infra Section I.A.3.).

There is some debate about the frequency of the specialized circumstances described in the previous paragraph. For example, Professors Jonathan Baker, Nancy Rose, Steven Salop, and Fiona Scott Morton noted that “common assumptions that EDM merger benefits are inevitable . . . and that EDM can be presumed to be merger-specific” are not supported by economic reasoning.38Jonathan B. Baker, Nancy L. Rose, Steven C. Salop & Fiona Scott Morton, Comments Letter on the Draft Vertical Merger Guidelines, at 31 (Feb. 24, 2020), https://perma.cc/W9MN-X3W9. American Antitrust Institute President Diana Moss suggests “[t]here is a well-established case for caution regarding EDM, which is rooted in the restrictive assumptions underlying the theory.”39American Antitrust Institute, Comment Letter on Draft Vertical Merger Guidelines, at 10 (Feb. 25, 2020), https://perma.cc/LNQ6-8UX9.

Contrary to these assertions, a vertical merger is likely to result in EDM if the cost to the upstream firm of supplying an input to the downstream firm (i.e., exclusive of markup) is less than the cost to the downstream firm of acquiring the same input from an unintegrated firm. Since an unintegrated firm typically will charge a markup above its costs, this condition will generally apply. While some types of contracts, such as two-part tariffs, can mitigate the double marginalization problem outside of vertical integration,40See infra Section I.A.3. there is no evidence that firms that have not already implemented such contracts are likely to be able to fully eliminate the double margin by changing contracting practices.41See Daniel P. O’Brien, The Antitrust Treatment of Vertical Restraints: Beyond the Possibility Theorems, in Swedish Competition Authority, The Pros and Cons of Vertical Restraints 40, 63 (2008) (“The use of nonlinear contracts can mitigate double-marginalization, but it does not necessarily eliminate it.”). In fact, the empirical literature supports the contrary conclusion—namely, that vertical integration via contract is an imperfect substitute for vertical integration via merger.42See United States v. AT&T, Inc., 916 F.3d 1029, 1038 (D.C. Cir. 2019) (describing EDM likely to result from the merger); Gregory S. Crawford, Robin S. Lee, Michael D. Whinston & Ali Yurukoglu, The Welfare Effects of Vertical Integration in Multichannel Television Markets, 86 Econometrica 891, 893–94 (2018) (finding substantial savings from integration in the cable industry); Lafontaine & Slade, supra note 28, at 649 (summarizing strong empirical support for inefficiencies associated with contracting); see also discussion of the GM/Fisher merger infra Part III. The Vertical Merger Guidelines endorse this perspective in noting that “[t]he Agencies do not, however, reject the merger specificity of the elimination of double marginalization solely because it could theoretically be achieved but for the merger.”43Dep’t of Justice & Fed. Trade Comm’n, supra note 3, at 12.

Most retrospective studies find that vertical integration benefitted consumers, and few show harmful effects.44See Francine Lafontaine & Margaret Slade, Franchising and Exclusive Distribution: Adaptation and Antitrust, in II Oxford Handbook of International Antitrust Economics 387 (Roger D. Blair & D. Daniel Sokol eds., 2014) (providing a literature review); LaFontaine & Slade, supra note 28, at 677 (“[O]verall a fairly clear empirical picture emerges. The data appear to be telling us that efficiency considerations overwhelm anticompetitive motives in most contexts. Furthermore, even when we limit attention to natural monopolies or tight oligopolies, the evidence of anticompetitive harm is not strong.”). Merger retrospectives often measure the performance of merged firms against a set of similarly situated control firms. Such studies may be limited to observing the overall effects of a vertical merger on merging firms and may be unable to distinguish between various procompetitive and anticompetitive effects.45But see Fernando Luco & Guillermo Marshall, The Competitive Impact of Vertical Integration by Multiproduct Firms, 110 Am. Econ. Rev. 2041, 2043 (2020) (measuring separately the effects of vertical integration on integrated and nonintegrated firms, finding unintegrated products increased in price by 1.2 to 1.5 percent, while prices for integrated products decreased by 0.8 to 1.2 percent). Nonetheless, the literature suggests that EDM is very likely to contribute significantly to the procompetitive effects of most vertical mergers.46See Cooper et al., supra note 29, at 648 (surveying twenty-two empirical papers, which “appear to provide strong support for the proposition that vertical integration/vertical restraints often help solve double markup problems”); Crawford et al., supra note 42, at 893–94 (describing an estimated structural model of the cable industry allowing a finding that “$0.79 of each dollar of profit realized by its integrated partner is internalized . . . when integrated MVPDs and RSNs bargain with each other” and that the overall effect of vertical integration, even in the absence of program access rules, “is to increase consumer and total welfare”); Panos Kouvelis, Drug Pricing for Competing Pharmaceutical Manufacturers Distributing Through a Common PBM, 27 Prod. Oper. Mgmt. 3799 (2018) (finding “when the price sensitivity of the PBM’s market size is sufficiently small, unless the vertical integration is associated with a sufficient increase in the market base, social welfare decreases after the integration due to the profit loss from the non‐integrated branded drug manufacturers. When the price sensitivity of the PBM’s market size is relatively large, the elimination of double marginalization benefits plan enrollees and significantly expands the PBM’s price‐driven market size, which leads to a higher social welfare in the post‐integration model”); Gunther Glenk & Stefan Reichelstein, Synergistic Value in Vertically Integrated Power‐to‐Gas Energy Systems, 29 Prod. Oper. Mgmt. 526, 526–28 (2020) (identifying vertical integration effectiveness in electric energy); Ricard Gil, Does Vertical Integration Decrease Prices? Evidence from the Paramount Antitrust Case of 1948, 7 Amer. Econ. J. 162 (2015). On the limits of the assumptions on EDM see John Kwoka & Margaret Slade, Second Thoughts on Double Marginalization, Antitrust Mag., Spring 2020, at 51; Jaideep Shenoy, An Examination of the Efficiency, Foreclosure, and Collusion Rationales for Vertical Takeovers, 58 Mgmt Sci. 1482, 1500 (2012) (“Collectively, our findings indicate that firms use corporate takeovers to expand their vertical boundaries consistent with an efficiency improvement rationale as predicted by the transaction cost economics and property rights theories.”).

EDM benefits are likely to be largest when the upstream firm, prior to the merger, charges a large markup to the downstream firm it acquires.47See infra note 68 and accompanying text. Benefits may be smaller if the merging firms already engage in some form of nonlinear contracting, or if the upstream firm is capacity constrained.

In summary, unlike horizontal mergers, vertical mergers induce a procompetitive unilateral effect in addition to any such anticompetitive effects and in addition to procompetitive productive efficiencies.

2. Efficiencies

Often commentary on the procompetitive effects of vertical mergers focuses on EDM. Though EDM is important, there are many other potential procompetitive effects that should be considered. These efficiencies play a role in both vertical mergers and mergers of complementary or adjacent products.48See, e.g., Annabelle Gawer & Rebecca Henderson, Platform Owner Entry and Innovation in Complementary Markets: Evidence from Intel, 16 J. Econ. & Mgmt. Strategy 1 (2007); Zhuoxin Li & Ashish Agarwal, Platform Integration and Demand Spillovers in Complementary Markets: Evidence from Facebook’s Integration of Instagram, 63 Mgmt. Sci. 3438 (2017). These efficiencies, while real both in terms of theory and empirics, often are not developed by the parties or credited by the Agencies. This “chicken and egg” problem hinders substantive development of efficiency arguments, both in litigation and during the Agencies’ merger review process.49See Christine S. Wilson, Comm’r, Fed. Trade Comm’n, Remarks on Breaking the Vicious Cycle: Establishing a Gold Standard for Efficiencies at Bates White Antitrust Webinar (June 24, 2020), https://perma.cc/88HA-K25L.

a. Reduction of Transaction Costs

Related to but distinct from EDM is the reduction of transaction costs through merger.50For EDM reviews outside of economics, see, for example, Gérard. P. Cachon & Patrick T. Harker, Competition and Outsourcing with Scale Economies, 48 Mgmt. Sci. 1314 (2002). Transaction costs explain why certain firms vertically integrate via merger rather than through contracts (markets).51See Mikko Ketokivi & Joseph T. Mahoney, Transaction Cost Economics As a Theory of Supply Chain Efficiency, 29 Prod. & Operations Mgmt. 1011, 1011 (2020) (“TCE [is] one of the most cited and applied organization theories in operations and supply chain management research . . . .”); see also Andy A. Tsay, John V. Gray, In Joon Noh & Joseph T. Mahoney, A Review of Production and Operations Management Research on Outsourcing in Supply Chains: Implications for the Theory of the Firm, 27 Prod. & Operations Mgmt. 1177, 1179–80 (2018). Nobel laureate Oliver Williamson defined a transaction as an event “when a good or service is transferred across a technologically separable interface. One stage of [processing or assembly] activity terminates and another begins.”52Oliver E. Williamson, The Economics of Organization: The Transaction Cost Approach, 87 Am. J. Soc. 548, 552 (1981). Thus, there is a choice of “make” or “buy” to reduce transaction costs. 53See Soon Ang & Detmar W. Straub, Production and Transaction Economies and IS Outsourcing: A Study of the U.S. Banking Industry, 22 MIS Q. 535, 537 (1998); Michael J. Leiblein & Douglas J. Miller, An Empirical Examination of Transaction and Firm-Level Influences on the Vertical Boundaries of the Firm, 24 Strategic Mgmt. J. 839, 848 (2003). Of course, a firm can pursue both strategies. See Anne Parmigiani, Why Do Firms Both Make and Buy? An Investigation of Concurrent Sourcing, 28 Strategic Mgmt. J. 285, 285 (2007).

The conditions under which transaction costs occur will vary with the particular governance mechanism used for a given transaction’s economic consequence.54See Williamson, supra note 8. Those organizations that can reduce transaction costs are more likely to create more value for themselves.

The theory that vertical integration may beneficially eliminate transaction costs first emerged in the 1970s, although its origins belong to Professor Ronald Coase.55See Oliver E. Williamson, Vertical Integration, in 4 The New Palgrave: A Dictionary of Economics 807, 809 (John Eatwell et al. eds., 1987) (“Although this [TCE] conception of the firm-as-governance-structure was first advanced fifty years ago (Coase, 1937), it lacked operationality and languished for most of the next thirty-five years (Coase, 1972). The past fifteen years [1972–1987], by contrast, have witnessed renewed attention to and operational headway on transaction cost matters.”). See generally Williamson, supra note 8; R. H. Coase, The Nature of the Firm, 4 Economica 386 (1937); Paul Joskow, Vertical Integration and Long-term Contracts: The Case of Coal-burning Electric Generating Plants, 1 J.L. Econ. & Org. 33 (1985); Klein et al., supra note 8; Oliver E. Williamson, The Vertical Integration of Production: Market Failure Considerations, 61 Am. Econ. Rev. 112 (1971). Empirical literature followed,56See, e.g., Jeffery T. Macher & Barak D. Richman, Transaction Cost Economics: An Assessment of Empirical Research in the Social Sciences, 10 Bus. & Pol. 1 (2008); Scott E. Masten, Reaffirming Relationship-Specific Investments: Comments on Miwa and Ramseyer’s ‘Rethinking Relationship-Specific Investments’, 98 Mich. L. Rev. 2668, 2675 (2000) (“The empirical literature examining the determinants of organizational form and contract design is extensive, certainly far too large to review here. Suffice it to say, surveys of the literature have all come to virtually the same conclusion, namely, that transaction-cost economics has been profoundly successful empirically.”); Howard A. Shelanski & Peter G. Klein, Empirical Research in Transaction Cost Economics: A Review and Assessment, 11 J. L. Econ. & Org. 335 (1995). as did literature focused on antitrust-related issues.57See, e.g., Lafontaine & Slade, supra note 28; Alan J. Meese, Robert Bork’s Forgotten Role in the Transaction Cost Revolution, 79 Antitrust L.J. 953, 960–61 (2014) (providing an overview). For an empirical review, see infra note 227 (discussing the factors considered in determining vertical merger policy). This literature identified that, under certain circumstances, vertical integration could eliminate transaction costs (particularly by addressing issues of specificity, uncertainty, and complexity) and thereby increase consumer welfare.58See Lafontaine & Slade, supra note 28, at 649 (summarizing literature on transaction costs models).

The premise behind the reduction of transaction costs through merger is that such integration is needed under a particular set of circumstances. Assume that assets are cospecialized. The more cospecialized the asset, the greater the need to have vertical integration. The more that a firm outsources cospecialized investments, the greater the likelihood of higher transaction costs due to holdup.59See Nicholas Argyres, Joseph T. Mahoney & Jackson Nickerson, Strategic Responses to Shocks: Comparative Adjustment Costs, Transaction Costs, and Opportunity Costs, 40 Strategic Mgmt. J. 357, 365 (2019). The possibility of such holdup may be factored into the pricing of contracts across firms or may cause a vertical partner to be chilled from making cospecialized investments. In contrast, outsourcing is more likely when transaction costs are lower.60There are of course hybrid organizational forms as well. See, e.g., Janet E.L. Bercovitz, The Option to Expand: The Use of Multi-Unit Opportunities to Support Self-Enforcing Agreements in Franchise Relationships, 1 Acad. Mgmt. Proc. Y1 (2002); Bryan Borys & David B. Jemison, Hybrid Arrangements As Strategic Alliances: Theoretical Issues in Organizational Combinations, 14 Acad. Mgmt. Rev. 234, 235 (1989).

b. Reduction of Asymmetric Risk

Vertical integration is a way to manage and mitigate risk, which may be asymmetric due to contractual incompleteness.61See Sanford J. Grossman & Oliver D. Hart, The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration, 94 J. Pol. Econ. 691, 717 (1986); Oliver D. Hart & John Moore, Property Rights and the Nature of the Firm, 98 J. Pol. Econ. 1119, 1120 (1990). Asymmetric risk also impacts the possibility of holdup or contractual renegotiation.62See George Baker, Robert Gibbons & Kevin J. Murphy, Informal Authority in Organizations, 15 J.L. Econ. & Org. 56, 59 (1999); Eric Maskin & John Moore, Implementation and Renegotiation, 66 Rev. Econ. Stud. 39, 52 (1999); Ilya Segal & Michael D. Whinston, The Mirrlees Approach to Mechanism Design with Renegotiation (With Applications to Hold-Up and Risk Sharing), 70 Econometrica 1, 1 (2002). Due to the incompleteness of contracts, one party may be more risk averse with respect to contracting than the other. This risk is inherent in the supply chain process and is exacerbated by varying levels of ownership. Vertical integration by merger solves these asymmetric risk problems.63See René Aïd, Gilles Chemla, Arnaud Prochet & Nizar Touzi, Hedging and Vertical Integration in Electricity Markets, 57 Mgmt. Sci. 1438, 1449–50 (2011) (discussing reduction of asymmetric risk).

The risk uncertainty of a manufacturer may affect how it distributes its product downstream.64See V. Kasturi Rangan, E. Raymond Corey & Frank Cespedes, Transaction Cost Theory: Inferences from Clinical Field Research on Downstream Vertical Integration, 4 Org. Sci. 454, 454 (1993) (“[C]hannel investments are influenced by a firm’s uncertainty absorption mechanism . . . .”). The chosen options will differ based on a firm’s resources and strategy. Some firms may use distributors, an approach that creates various risks like principal-agent problems. Firms averse to these risks may want to mitigate them by vertically integrating forward. Financial vertical integration may improve a firm’s ability to achieve sales targets or to reap the rewards of promotional activities.65See Wei Guan & Jakob Rehme, Vertical Integration in Supply Chains: Driving Forces and Consequences for a Manufacturer’s Downstream Integration, 17 Supply Chain Mgmt. 187, 189 (2012); George John & Barton A. Weitz, Forward Integration into Distribution: An Empirical Test of Transaction Cost Analysis, 4 J.L. Econ. & Org. 337, 341 (1988). Thus, downstream integration offers more control for a manufacturer over marketing practices, and increased control reduces uncertainty.

c. Learning-by-Doing

A knowledge‐based view of the firm, a view used in the management literature, stresses the role that knowledge plays in firm performance. Knowledge develops via learning-by-doing—an approach based on experiential learning within the firm.66See, e.g., Linda Argote, Organizational Learning: Creating, Retaining and Transferring Knowledge 38 (2d ed. 2013); Olav Sorenson, Interdependence and Adaptability: Organizational Learning and the Long-Term Effect of Integration, 49 Mgmt. Sci. 446, 446 (2003) (discussing “learning by doing” based on asset specificity). If used effectively, learning-by-doing improves firm outcomes.67See Will Mitchell, J. Myles Shaver & Bernard Yeung, Foreign Entrant Survival and Foreign Market Share: Canadian Companies’ Experience in United States Medical Sector Markets, 15 Strategic Mgmt. J. 555, 565 (1994). Organizational design plays a role in these outcomes. Firms with greater internal knowledge can benefit from greater vertical integration because of this increased knowledge.68See Rebecca Henderson & Ian Cockburn, Scale, Scope, and Spillovers: The Determinants of Research Productivity in Drug Discovery, 27 RAND J. Econ. 32, 33 (1996); Jeffrey T. Macher & Christopher Boerner, Technological Development at the Boundaries of the Firm: A Knowledge‐Based Examination in Drug Development, 33 Strategic Mgmt. J. 1016, 1032 (2012) (“Holding firm experience constant, insourcing fosters control and facilitates communication in ways that outsourcing has difficulty matching.”); Jeffrey T. Macher, Technological Development and the Boundaries of the Firm: A Knowledge-Based Examination in Semiconductor Manufacturing, 52 Mgmt. Sci. 826, 832 (2006).

The intuition is that the more specialized a firm becomes, the more constrained it is in its ability to coordinate effectively across different interdependent stages of production in a supply chain.69See David J. Teece, Firm Organization, Industrial Structure, and Technological Innovation, 31 J. Econ. Behav. & Org. 193, 222 (1996) (identifying “firm organization . . . [as] an important determinant of innovation”). In this context, something short of integration—like a joint venture that is vertical in nature70See John Alan Stuckey, Vertical Integration and Joint Ventures in the Aluminum Industry 149 (1983) (explaining a joint venture consists of “two or more separate groups [that] jointly participate as co-owners of a producing organization” while “each joint venturer continues to exist as . . . independent of the joint-venture firm”). or perhaps a strategic alliance—may be less efficient than vertical integration. In these settings, vertical integration is superior because extensive knowledge sharing and the coordination of interdependent tasks enabled by higher levels of internal knowledge enable the extraction of greater benefits. 71See Rahul Kapoor, Persistence of Integration in the Face of Specialization: How Firms Navigated the Winds of Disintegration and Shaped the Architecture of the Semiconductor Industry, 24 Org. Sci. 1195, 1198 (2013).

d. Knowledge Transfers

Vertical mergers also may generate efficiencies by facilitating the transfer of knowledge.72See Fredrik Tell, Knowledge Integration and Innovation: A Survey of the Field, in Knowledge Integration and Innovation: Critical Challenges Facing International Technology-Based Firms 20 (Christian Berggren et al. eds., 2011); Enghin Atalay, Ali Hortaçsu & Chad Syverson, Vertical Integration and Input Flows, 104 Am. Econ. Rev. 1120, 1146 (2014); Robert M. Grant, Prospering in Dynamically-Competitive Environments: Organizational Capability as Knowledge Integration, 7 Org. Sci. 375, 380 (1996); Gabriel Natividad, Integration and Productivity: Satellite-Tracked Evidence, 60 Mgmt. Sci. 1698, 1717 (2014); Zheng Jane Zhao & Jaideep Anand, A Multilevel Perspective on Knowledge Transfer: Evidence From the Chinese Automotive Industry, 30 Strategic Mgmt. J. 959 (2009). Knowledge-based hierarchies are increasingly understood to add value to firms.73See Luis Garicano, Hierarchies and the Organization of Knowledge in Production, 108 J. Pol. Econ. 874, 875–76 (2000); Raaj K. Sah & Joseph E. Stiglitz, The Quality of Managers in Centralized Versus Decentralized Organizations, 106 Q.J. Econ. 289, 289 (1991). A number of theoretical papers argue that hierarchies require the integration of knowledge to be effective.74See, e.g., Yanhui Wu, Organizational Structure and Product Choice in Knowledge-Intensive Firms, 61 Mgmt. Sci. 1830 (2015). Within an organizational setting, the firm must acquire, gather, and process information.75See Masahiko Aoki, The Contingent Governance of Teams: Analysis of Institutional Complementarity, 35 Int’l Econ. Rev. 657, 658–60 (1994); Patrick Bolton & Mathias Dewatripont, The Firm as a Communication Network, 109 Q.J. Econ. 809, 809 (1994); Garicano, supra note 73, at 874; Timothy Van Zandt, Real-Time Decentralized Information Processing as a Model of Organizations with Boundedly Rational Agents, 66 Rev. Econ. Stud. 633, 633 (1999); Wu, supra note 74; Kevin Zheng Zhou & Caroline Bingxin Li, How Knowledge Affects Radical Innovation: Knowledge Base, Market Knowledge Acquisition, and Internal Knowledge Sharing, 33 Strategic Mgmt. J. 1090, 1092 (2012). This body of work suggests that an acquisition is valuable only if the acquirer can internalize and integrate the knowledge of the target.76See Bruno Cassiman, Massimo G. Colombo, Paola Garrone & Reinhilde Veugelers, The Impact of M&A on the R&D Process: An Empirical Analysis of the Role of Technological- and Market-Relatedness, 34 Res. Pol’y 195, 198 (2005); Marianna Makri, Michael A. Hitt & Peter J. Lane, Complementary Technologies, Knowledge Relatedness, and Invention Outcomes in High Technology Mergers and Acquisitions, 31 Strategic Mgmt. J. 602, 603 (2010).

The ability to direct knowledge transfer depends on both intensity and location of the knowledge transfer. Knowledge creation and transfer will work differently if outsourced outside the firm or if undertaken within the firm.77See generally George von Krogh, Kazuo Ichijo & Ikujiro Nonaka, Enabling Knowledge Creation: How to Unlock the Mystery of Tacit Knowledge and Release the Power of Innovation (2000); Riikka Mirja Sarala, Paulina Junni, Cary L. Cooper & Shlomo Yedidia Tarba, A Sociocultural Perspective on Knowledge Transfer in Mergers and Acquisitions, 42 J. Mgmt. 1230 (2016); Henrik Bresman, Julian Birkinshaw & Robert Nobel, Knowledge Transfer in International Acquisitions, 41 J. Int’l Bus. Stud. 5 (2010). Within the firm, knowledge transfer requires a different orientation, and it may be more difficult to replicate this set of relationships across organizations.

e. Reduction of Information Leakage Due to the Use of Trade Secrets

Firms may be unwilling to coordinate fully with upstream or downstream partners because of potential information leakage to competitors or would-be competitors. With vertical integration via merger, a firm need not be as concerned with information leakage and the loss of trade secrets. For this reason, vertical mergers may boost firm productivity with regard to critical high value products and processes.78See Sharon Novak & Scott Stern, Complementarity Among Vertical Integration Decisions: Evidence from Automobile Product Development, 55 Mgmt. Sci. 311, 312 (2009).

f. Reducing Inventory Costs

Inventory costs can be an important driver of total costs.79See Timothy F. Bresnahan & Peter C. Reiss, Dealer and Manufacturer Margins, 16 RAND J. Econ. 253, 264 (1985). Vertical integration may facilitate faster optimization and control over inventory,80See Diane J. Reyniers, The Effect of Vertical Integration on Consumer Price in the Presence of Inventory Costs, 130 Eur. J. Operational Res. 83, 88 (2001) (discussing how vertical integration may reduce inventory costs). and it also may reduce forecast bias.81See Xiang Wan & Nadia R. Sanders, The Negative Impact of Product Variety: Forecast Bias, Inventory Levels, and the Role of Vertical Integration, 186 Int’l J. Prod. Econ. 123, 123–24 (2017). Empirical work suggests that vertical integration can improve operational performance through better inventory scheduling.82See Hong Chen, Murray Z. Frank & Owen Q. Wu, What Actually Happened to the Inventories of American Companies Between 1981 and 2000?, 51 Mgmt. Sci. 1015, 1015–17 (2005); John Stuckey & David White, When and When Not to Vertically Integrate, 34 Sloan Mgmt. Rev. 71 (1993). Certainly some firms—like Walmart, Amazon, and Toyota—are very effective in creating complex supply chains for just-in-time delivery. However, other firms are less effective at creating a lean supply chain system. For these other firms, the use of an internal transport hub for both production and logistics would make inventory scheduling easier.83See Richard A. D’Aveni & David J. Ravenscraft, Economies of Integration versus Bureaucracy Costs: Does Vertical Integration Improve Performance?, 37 Acad. Mgmt. J. 1167, 1170 (1994). Indeed, internalization of the coordination functions may improve information flow or create efficiencies due to technological interdependencies in the production process.84See Abbie Griffin & John R. Hauser, Patterns of Communication Among Marketing, Engineering, and Manufacturing—A Comparison Between Two Product Teams, 38 Mgmt. Sci. 360 (1992).

Information sharing across firms in a supply chain may be valuable to reduce inventory costs and other related inefficiencies.85See Hau L. Lee, Kut C. So & Christopher S. Tang, The Value of Information Sharing in a Two-Level Supply Chain, 46 Mgmt. Sci. 626, 627 (2000). However, effective sharing must include effective management and coordination across information technology (“IT”) infrastructures.86See Henk Akkermans, Paul Bogerd, Enver Yücesan & Luk N. van Wassenhove, The Impact of ERP on Supply Chain Management: Exploratory Findings From a European Delphi Study, 146 Eur. J. Operational Res. 284, 300 (2003); Eric K. Clemons & Bruce W. Weber, London’s Big Bang: A Case Study of Information Technology, Competitive Impact, and Organizational Change, 6 J. Mgmt. Info. Sys. 41, 46–47 (1990). The more difficult it is to address disparate IT infrastructures, the more difficult it may be to achieve efficiencies in inventory management. These effects vary by firm IT due to the specific assets within a given firm. With the right set of assets, vertical integration—when a single firm has a more unified IT infrastructure—is efficient.87See Gautam Ray, Ling Xue & Jay B. Barney, Impact of Information Technology Capital on Firm Scope and Performance: The Role of Asset Characteristics, 56 Acad. Mgmt. J. 1125, 1142 (2013) (noting that “in firms with narrowly valuable assets, the electronic brokerage effect of IT capital is likely to dominate, and IT capital is likely to facilitate more vertical and product-market specialization, in ways that are consistent with transaction cost economics; and in firms with broadly valuable assets, the electronic integration effect of IT capital is likely to dominate, and IT capital is likely to facilitate more vertical integration and product-market diversification, in ways that are consistent with the resource-based view”). Thus, the effective use of IT infrastructure within the same firm allows for reallocating excess IT-related capacity within other units of the firm to reduce inventory and other costs.88See Hüseyin Tanriverdi, Performance Effects of Information Technology Synergies in Multibusiness Firms, 30 MIS Q. 57, 58 (2006).

g. Research and Development and Innovation-Related Synergies

One driver of vertical mergers may be research and development synergies. A series of finance papers suggests that complementary assets create efficiencies for merged firms.89See Jan Bena & Kai Li, Corporate Innovations and Mergers and Acquisitions, 69 J. Fin. 1923, 1955 (2014); Matthew J. Higgins & Daniel Rodriguez, The Outsourcing of R&D Through Acquisition in the Pharmaceutical Industry, 80 J. Fin. Econ. 351, 381 (2006); Gerard Hoberg & Gordon M. Phillips, Product Market Synergies and Competition in Mergers and Acquisitions: A Text-Based Analysis, 23 Rev. Fin. Stud. 3773, 3808 (2010); Simi Kedia, S. Abraham Ravid & Vincente Pons, When Do Vertical Mergers Create Value?, 40 Fin. Mgmt. 845, 872 (2011); Gordon M. Phillips & Alexei Zhdanov, R&D and the Incentives from Merger and Acquisition Activity, 26 Rev. Fin. Stud. 34, 71–72 (2013). This literature is premised on the important underlying assumption that contractual integration short of a merger—through a strategic alliance, bilateral contracting, or corporate venture capital—is insufficient to achieve such efficiencies.

The nature of knowledge transfer within a firm’s boundaries partly explains why acquisitions and contractual arrangements accomplish different results.90See David J. Teece, Dynamic Capabilities and Strategic Management: Organizing For Innovation and Growth 171 (2009); Henry W. Chesbrough & David J. Teece, When Is Virtual Virtuous? Organizing for Innovation, 74 Harv. Bus. Rev. 65 (1996); David J. Teece, Gary Pisano & Amy Shuen, Dynamic Capabilities and Strategic Management, 18 Strategic Mgmt. J. 509 (1997). For example, in a study on the pharmaceutical industry, internal knowledge coupled with external acquisition led to greater consumer welfare.91See John Hagedoorn & Ning Wang, Is There Complementarity or Substitutability Between Internal and External R&D Strategies?, 41 Res. Pol’y 1072, 1073 (2012) (“[I]nternal R&D and external R&D, through either R&D alliances or R&D acquisitions, are complementary innovation activities at higher levels of in-house R&D investments, whereas at lower levels of in-house R&D efforts, internal and external R&D turn out to be substitutive strategic options.”); Jaideep C. Prabhu, Rajesh K. Chandy & Mark E. Ellis, The Impact of Acquisitions on Innovation: Poison Pill, Placebo, or Tonic?, 69 J. Mktg. 114, 126–27 (2005) (“Acquisitions provide a means to access external knowledge that can be difficult or even impossible to create through internal sources.”). But see Colleen Cunningham, Florian Ederer & Song Ma, Killer Acquisitions 1–3 (April 22, 2020) (unpublished manuscript), https://perma.cc/RUU8-LH6N (identifying mechanisms by which mergers might kill off potential competitors in the pharmaceutical industry). Similarly, technological relatedness creates increased efficiencies.92See Gautam Ahuja & Riitta Katila, Technological Acquisitions and the Innovation Performance of Acquiring Firms: A Longitudinal Study, 22 Strategic Mgmt. J. 197, 215 (2001); Cassiman et al., supra note 76, at 213; Panos Desyllas & Alan Hughes, Do High Technology Acquirers Become More Innovative?, 39 Res. Pol’y 1105, 1117 (2010); Joshua Sears & Glenn Hoetker, Technological Overlap, Technological Capabilities, and Resource Recombination in Technological Acquisitions, 35 Strategic Mgmt. J. 48, 49–51 (2014).

We recognize that not all mergers lead to the anticipated efficiencies. As one article summarizes:

Building a new competitive capability via technology acquisitions is a multi-stage process in which the acquisition itself is simply the first step. Acquiring firms obtain valuable knowledge through acquisitions of target firms. Then, they must utilize the acquired knowledge for their subsequent services or products. Otherwise, the acquired knowledge is simply hoarded within the acquiring firms, and they fail to actualize the value of the acquired knowledge.93Seungho Choi & Gerry McNamara, Repeating a Familiar Pattern in a New Way: The Effect of Exploitation and Exploration on Knowledge Leverage Behaviors in Technology Acquisitions, 39 Strategic Mgmt. J. 356, 357 (2018).

Overall, firm cultures differ, and the agility of startups is not always present in large firms.

h. Investment Coordination

Lack of information sharing creates the potential for a lack of coordination within a supply chain.94See Chenyu Yang, Vertical Structure and Innovation: A Study of the SoC and Smartphone Industries 1 (Sept. 1, 2019) (unpublished manuscript), https://perma.cc/E8QT-E52Z (studying vertical integration with chipset systems in smartphone industries). Investment coordination within a firm is a way to solve this information problem and may justify vertical integration.95See Robert Gibbons, Taking Coase Seriously, 44 Admin. Sci. Q. 145 (1999). Coordination risk stems from the fact that an individual firm’s decisions contribute to a collective vertical outcome. Because those individual firms may employ different decisional rules, and because the choice of decisional rule is frequently opaque, supply chain instability may result.

The classic business school “beer game”96See, e.g., Jay W. Forrester, Industrial Dynamics 357–58 (1961); Lisa Ellram, Introduction to the Forum on the Bullwhip Effect in the Current Economic Climate, 46 J. Supply Chain Mgmt. 3 (2010).—known in academic literature as the “bullwhip effect”97See, e.g., Rachel Crosen, Karen Donohue, Elena Katok & John Sterman, Order Stability in Supply Chains: Coordination Risk and the Role of Coordination Stock, 23 Prod. & Operations Mgmt. 176 (2014); Ellram, supra note 96, at 3; Kimberly M. Thompson & Nima D. Badizadegan, Valuing Information in Complex Systems: An Integrated Analytical Approach to Achieve Optimal Performance in the Beer Distribution Game, 3 IEEE Access 2677, 2677–78 (2015).—exemplifies this phenomenon. The beer game explores how an entire supply chain (suppliers, manufacturers, and customers), purchasing agents, and marketing agents may have an incomplete view of actual demand for beer because of a lack of information. Each level within the supply chain can impact the entire supply chain if that level orders too much or too little beer. Thus, there is an interdependency of decision-making across each level of the vertical chain. Just so, intrafirm investment coordination may produce efficiencies because the agency costs of coordination within the firm may be reduced below the transaction costs of coordination across multiple actors in multiple firms.98See Crosen et al., supra note 97, at 194 (“[T]he notion of ‘optimal’ behavior is contingent on people’s assumptions about the thinking and behavior of the other agents with whom they interact. If a person believes that their counterparts will behave in an unpredictable and capricious fashion, this may lead to further instability in the supply chain.”). One may assume from these findings that it is easier through incentive alignment within a single firm, such as through financial rewards, than alignment across firms.

3. Do Mergers and Contracts Produce the Same Benefits?

Three contractual alternatives to complete integration by merger may yield some or all of the same economic benefits as vertical mergers when successfully implemented by unintegrated, vertically related firms.99See Roger D. Blair & Amanda K. Esquibel, Maximum Resale Price Restraints in Franchising, 65 Antitrust L.J. 157, 176–77 (1996); see also Roger D. Blair & David L. Kaserman, Optimal Franchising, 49 S. Econ. J. 494 (1982); Roger D. Blair & David L. Kaserman, Uncertainty and the Incentive for Vertical Integration, 45 S. Econ. J. 266 (1978).

First, maximum resale prices may, in certain circumstances, allow unintegrated firms to eliminate double marginalization via contract. If such a contract is possible, the upstream firm would optimally set a maximum resale price equal to the price a vertically integrated firm would charge. At the same time, the upstream firm would compensate the downstream firm via lump-sum payment so that the downstream firm is no worse off than it would be absent the contract. Referring back to Figure 1,100Supra Section I.A.1. a maximum resale price of P2 would achieve the benefits of EDM. The downstream retailer would then sell Q2 at P2. The upstream firm would earn a variable profit of (w1 – MCP)Q2, while the downstream firm would earn a variable profit of zero; the upstream firm’s profit can then be shared with the downstream firm via a lump-sum payment. The combined profit would equal the maximum profit that a vertically integrated firm could earn.101The integrated firm’s profit is (P2 – MCR – MCP)Q2 while the unintegrated firms’ profits sum to (w1 – MCP)Q2. Since P2 = w1 + MCR, these profits are identical. Of course, prior to State Oil Co. v. Kahn, 522 U.S. 3 (1997), maximum resale prices were per se illegal under Albrecht v. Herald Co., 390 U.S. 145 (1968).

A second, closely related contractual alternative is a sales quota. The upstream firm can sell its output to the downstream firm at a price of w1 on the condition that the downstream firm purchases at least Q2 units. Again, such a contract may require a lump-sum payment from the upstream firm to induce the downstream firm to agree to the contract. Referring again to Figure 1, the only way the downstream firm can sell Q2 units is to set a price of P2. Under an optimal sales quota contract, the upstream firm’s variable profits would be (w1 – MCP)Q2, while the downstream firm would earn zero variable profit.

A third and final contractual alternative is a two-part tariff. The upstream and downstream firms could agree to a contract in which the downstream firm pays a lump-sum license fee no greater than (P2 – MCR – MCP)Q2 in exchange for the right to purchase as many units as it would like from the upstream firm at a price equal to the upstream firm’s marginal cost, MCP.

Maximum resale prices, sales quotas, and two-part tariffs partially replicate EDM’s effects to the benefit of consumers. Hence, when any such contract is observed between two unintegrated firms, it is very likely to be efficient. Importantly, the inverse—that a lack of such contracting implies the inefficiency of vertical integration—is false. In practice, the obstacles that confront two unintegrated firms seeking to reach agreement on such a contract may often be significant.102See Gregory J. Werden & Luke M. Froeb, Comment Letter on Proposed Vertical Merger Guidelines 1 (Feb. 6, 2020), https://perma.cc/PW2P-5VNA (“[I]t is essential to appreciate that vertical mergers solve coordination problems that are solved less well, or not at all, by contracts.”). To take just one example, optimal implementation of a maximum resale price arrangement would require full knowledge of both the demand curve for the final good and both firms’ cost curves to set the maximum price. Any antitrust practitioner knows how difficult it is to project costs and demand across a range of counterfactual scenarios, as would be required for complete contracting. Thus, it is likely that for many unintegrated firms, efficient contracting is either impossible or prohibitively costly.

Instead, some commentators seem to embrace the idea that a lack of contracting indicates that there is no conceivable gain to greater integration. For instance, Professors Baker, Rose, Salop, and Scott Morton state that “[i]f in advance of the merger the parties never considered contracting to eliminate double marginalization, that fact may suggest that EDM would not achieve substantial benefits.”103Baker et al., supra note 4, at 15. This suggestion overlooks innocuous explanations for lack of premerger contracting, including insurmountable information asymmetries or contracting costs. In contrast, EDM is not difficult for a fully vertically integrated firm to realize: all that is required is for the upstream firm to sell its output to the downstream firm at cost.

Putting aside the minor question of how firms could possibly demonstrate the impossibility of achieving a certain type of contract, there appears to be no basis for an inference that because certain types of contracts are theoretically possible, EDM generated by merger is irrelevant.104 To do so would apply an even more stringent standard for merger specificity than the Horizontal Merger Guidelines, which state “[o]nly alternatives that are practical in the business situation faced by the merging firms are considered in making this determination [of merger specificity]. The Agencies do not insist upon a less restrictive alternative that is merely theoretical.” Horizontal Merger Guidelines, supra note 31, at 30.

In summary, while there is convincing theoretical and empirical evidence that vertical contracts can efficiently eliminate double marginalization, the inverse argument—that the absence of those contracts implies they are inefficient—is wrong. An alternative—and more likely—explanation for the inability to achieve EDM via contract is that implementing those contracts is difficult (e.g., because of informational asymmetries and contracting costs). Fortunately, the Vertical Merger Guidelines broadly endorse the merger specificity of EDM in saying that existing, premerger contracts are generally the appropriate baseline against which EDM must be measured.105See Dep’t of Justice & Fed. Trade Comm’n, supra note 3, at 11–12.

B. Anticompetitive Effects of Vertical Integration

The previous Section discussed how vertical mergers spur the merged firm to internalize a pricing externality, resulting in EDM. This Section discusses a related pricing externality: a higher price charged by the upstream firm to unintegrated downstream firms increases the profit of the integrated downstream firm. Once again, the upstream firm ignores this externality before merging, and it optimally accounts for it after merging. This incentive change creates the potential for anticompetitive effects to arise from vertical mergers. Potential anticompetitive effects include complete foreclosure, theories of two-level entry, and access to competitively sensitive information.

1. Raising Rivals’ Costs

If an upstream firm sells to multiple downstream firms, then its pricing to any particular downstream firm affects the profits of each other downstream firm. Consider an upstream firm U selling to downstream firms D1 and D2. Were U to increase the price it charges to D2, then D2 would optimally increase its final good price, causing it to lose customers.106The effect of input prices on a firm’s optimal output price is well-studied in the economics literature. See, e.g., Sonia Jaffe & E. Glen Weyl, The First-Order Approach to Merger Analysis, 5 Am. Econ. J.: Microeconomics 188 (2013) (developing a first order approximation of how upward pricing pressure generated by a horizontal merger is passed through to price); Nathan H. Miller, Marc Remer, Conor Ryan & Gloria Sheu, Upward Pricing Pressure as a Predictor of Merger Price Effects, 52 Int’l J. Indus. Org. 216 (2017) (finding that an own pass-through of one and cross pass-through of zero may reasonably approximate pass-through of incentives generated by horizontal mergers). If at least some of these lost customers switch to D1, then D1 will be more profitable than it was prior to U increasing the price it charged to D2.107To see this, note that D1 could increase its price until it had the same demand as it did prior to D2’s price increase, so that it would sell the same quantity at a greater margin. Of course, a smaller price increase may be even more profitable for D1.

When U and D1 are separately owned, U ignores the effect of its prices on D1’s profit, while a merger of U and D1 spurs U to internalize the effect of its price to D2 on the profits of D1. The result—higher prices to unintegrated downstream rivals—is often referred to as raising rivals’ costs (“RRC”). Analysis of the RRC pricing externality is often associated with Professor Steven Salop, who, along with coauthors, developed the foundations for RRC theories of harm in the 1980s.108See, e.g., Thomas G. Krattenmaker & Steven C. Salop, Anticompetitive Exclusion: Raising Rivals’ Costs to Achieve Power Over Price, 96 Yale L.J. 209 (1986); Steven C. Salop & David T. Scheffman, Raising Rivals’ Costs, 73 Am. Econ. Rev. 267 (1983).

The particular mechanism through which a vertical merger may result in RRC depends on the nature of the interactions between upstream and downstream firms. For example, business-to-business transactions are commonly conducted via bargaining in which both sides attempt to reach a mutually agreeable price (e.g., by exchanging offers). Naturally, the party that has less to lose from a breakdown in negotiations may be in a stronger bargaining position and thus able to demand more concessions from the party that has more to lose from a breakdown. As Professor William Rogerson explains, a vertical merger in this setting may result in RRC because it “affects the disagreement payoff of the upstream firm when it negotiates with a rival downstream firm. Its disagreement payoff is increased because it takes into account the extra profit that its own downstream affiliate will earn” in the event of a bargaining breakdown.109William P. Rogerson, Modelling and Predicting the Competitive Effects of Vertical Mergers: The Bargaining Leverage Over Rivals (BLR) Effect, 53 Canadian J. Econ. 407, 409 (2020).

Bargaining models have been prominent in antitrust analyses of several recent vertical mergers between upstream video content providers and downstream multichannel video programming distributors (“MVPDs”).110Id. at 410–11. In AT&T, the DOJ contended that owning AT&T’s DirecTV service would increase Time Warner’s bargaining leverage in negotiations for its content with unintegrated MVPDs, as “[t]he alternative to an agreement in every negotiation with a rival MVPD would be better for the merged firm because without a deal, DirecTV would steal valuable video subscribers away from that rival.”111Post-Trial Brief of the United States at 1, United States v. AT&T Inc., 310 F. Supp. 3d 161 (D.D.C. 2018). In the DOJ’s view, this additional bargaining power would enable Time Warner to extract higher programming fees from unintegrated MVPDs, ultimately resulting in higher prices to consumers.

The Court found various flaws in the DOJ’s RRC theory of harm. These flaws included unrebutted findings that similar past vertical mergers did not result in price increases, disbelief that the improvement to AT&T’s bargaining leverage would be substantial, failure to account for AT&T’s long-term contract offers, and poor quality inputs to the DOJ’s expert’s model.112See AT&T, 310 F. Supp. 3d at 216 (endorsing defendants’ findings that three prior vertical transactions did not lead to price increases); id. at 224 (“[T]he lynchpin of Professor Shapiro’s testimony . . . is the assumption that a post-merger Turner would gain increased leverage by wielding a blackout threat that will be only somewhat less incredible.”); id. at 226 (“I agree with defendants, for the most part, that the inputs and assumptions of Professor’s Shapiro’s model are not sufficiently grounded in the evidence . . . .”); id. at 239–40 (summarizing long-term contract offers). Similar bargaining models have been successfully employed by the Agencies in horizontal health care mergers.113See Findings of Fact and Conclusions of Law, Saint Alphonsus Med. Ctr.–Namps, Inc. v. St. Luke’s Health Sys., No. 1:12-CV-00560-BLW, 2013 WL 5410057, at *19 (D. Idaho Sept. 25, 2013) (“The Acquisition will increase substantially St. Luke’s bargaining leverage with health plans.”).

RRC effects are likely to be of greatest concern when the merged firm has unintegrated downstream customers and when these customers sell products that are close substitutes for the merged firm’s own downstream product and have limited comparable alternatives to purchasing inputs from the merged firm. Absent these conditions, concerns about potential RRC effects are appropriately diminished.

2. Foreclosure

Early vertical merger enforcement was often premised on the concern that the merged firm would not buy or sell from unintegrated firms and that this practice was facially anticompetitive.114For a full discussion, see infra Section II.B. To take but one example, the Sixth Circuit upheld the FTC’s administrative blocking of a vertical merger between a cement manufacturer and a ready mix concrete firm in part because the merger would have increased the fraction of northeastern US cement demand derived from vertically integrated concrete companies from 39.6% to 46.3%, which the FTC and the Sixth Circuit deemed “extremely significant” and “anti-competitive.”115U.S. Steel Corp. v. Fed. Trade Comm’n, 426 F.2d 592, 601 (6th Cir. 1970). In the court’s view, “[t]he important consideration is that the acquired company would not be free to choose for itself who shall supply its needs solely on the basis of price, service and quality of goods because the acquiring company has the power to substitute its own suppliers.”116Id. The court—and contemporary practitioners—referred to the putative closing of a vertically integrated firm to unintegrated competitors as “foreclosure.”117Id. Some texts distinguish between input foreclosure, or declining to sell to unintegrated downstream firms, and customer foreclosure, or declining to buy from unintegrated upstream firms. This Section addresses both.

The logic of foreclosure as an antitrust theory of harm in these early vertical cases often rested on two assumptions: first, that vertical integration precludes dealings with unintegrated firms, and second, that the result of two vertically related firms dealing exclusively with each other is necessarily anticompetitive. There is little support for either assumption.