Introduction

More than any time in recent history—some would say in over a century—antitrust looms large in the public imagination and discussion.1Carl Shapiro suggested that “[n]ot since 1912, when Teddy Roosevelt ran for President emphasizing the need to control corporate power, have antitrust issues had such political salience.” Carl Shapiro, Antitrust in a Time of Populism, 61 Int.’l J. Indus. Org. 714, 715 (2018). Within the last several years, both scholars and popular commentators have focused on the decrease in competition and the increase in the level of concentration in the US economy, explaining its adverse impact on consumers, workers, innovation, and even income inequality.2See id. at 717–19. The concerns that the US economy is hurting on account of a lack of competition—and rising concentration—were powerfully captured in a 2016 Obama Administration Council of Economic Advisors report, “The Benefits of Competition and Indicators of Market Power.”3Council of Econ. Advisers, Benefits of Competition and Indicators of Market Power 4–6 (Apr. 2016), https://perma.cc/DMC2-MM4G. Since that report, the concerns about the decline of competition have gained bipartisan traction, raising the question of how we meet the challenges of this antitrust moment.

This Article outlines some initial observations and suggestions for revitalizing antitrust at this important time in our nation’s history. Part I discusses the decline of competition and the increase in the level of concentration in our economy and how these circumstances differ from the 1960s and 1970s when the Chicago School of antitrust criticized antitrust enforcement as untethered from economics. Part II evaluates two consequences of more concentrated markets—enhanced opportunities for coordination or collusion by incumbent firms and the impact of vertical mergers (e.g., between a supplier and distributor) on competition. Part III examines the role of monopolization law and the antitrust cases filed against Facebook and Google. This Article then concludes with some thoughts on how to respond to this critical moment for antitrust enforcement.

I. A Revolution in Thinking

In the 1960s, some commentators and antitrust enforcers rarified the role of small businesses as an end in and of itself, arguing that mergers of any notable size should be barred.4See, e.g., Sandeep Vaheesan, Two-and-a-Half Cheers for 1960s Merger Policy, HLS Antitrust Ass’n (Dec. 12, 2019), https://perma.cc/8WDQ-9NXS. In that era, mergers were generally not analyzed based on their likely competitive effects. Consider, for example, United States v. Von’s Grocery Co.,5384 U.S. 270 (1966). where the Supreme Court enjoined a merger of two grocery chains with a combined market share of just 7.5%.6Id. at 272. That decision famously represented a “big is bad” attitude and fueled the Chicago School of antitrust law that focused on actual economic consequences and critiqued such decisions.

Justice Stewart’s Von’s Grocery dissent anticipated the Chicago School critique, calling out the majority opinion for its lack of rigor. For starters, Justice Stewart commented that the opinion made “no effort to appraise the competitive effects of this acquisition in terms of the contemporary economy of the retail food industry in the Los Angeles area.”7Id. at 282 (Stewart, J., dissenting). Notably, Justice Stewart skewered the majority for adopting a per se rule against mergers in the face of any trend towards concentration, ignoring that small businesses were competing effectively against the larger chains and overlooking that there were not significant barriers to entry.8Id. at 283. Finally, Justice Stewart took a few shots at the majority’s overall approach, noting that “the emotional impact of a merger between the third and sixth largest competitors in a given market, however fragmented, is understandable, but that impact cannot substitute for the analysis of the effect of the merger on competition”9Id. at 304. and “[t]he sole consistency that I can find is that in litigation under [the antitrust laws], the Government always wins.”10Id. at 301.

The Chicago School critique, which was led in the 1970s and 1980s by leading scholars (and later judges) like Robert Bork, Richard Posner, and Frank Easterbrook, highlighted the importance of economic rigor and market realities.11See, e.g., Richard A. Posner, The Chicago School of Antitrust Analysis, 127 U. Pa. L. Rev. 925, 925 (1979). This critique paved the groundwork for the development of the joint merger guidelines adopted by both the Department of Justice (“DOJ”) and Federal Trade Commission (“FTC”) in 1992 and revised in 1997 and 2010, which set forth an economic foundation for merger review.12See U.S. Dep’t of Just. & Fed. Trade Comm’n, Horizontal Merger Guidelines (2010) [hereinafter 2010 Merger Guidelines], https://perma.cc/CUW8-4EFR; U.S. Dep’t of Just. & Fed. Trade Comm’n, Horizontal Merger Guidelines (1997) [hereinafter 1997 Merger Guidelines], https://perma.cc/K9WY-3TM7; U.S. Dep’t of Just. & Fed. Trade Comm’n, 1992 Merger Guidelines (1992), https://perma.cc/7JLP-BE3P. The 1992 Merger Guidelines were the first ones jointly adopted by the FTC and DOJ. Cf. Herbert J. Hovenkamp & Carl Shapiro, Horizontal Mergers, Market Structures, and Burdens of Proof, 127 Yale L.J. 1996, 2003 (2018) (discussing the application of economic principles under the 1982 merger guidelines). Notably, instead of suggesting that all increases in concentration would violate the antitrust laws, the guidelines adopted the Herfindahl-Hirschman Index (“HHI”) and a focus on the market shares of the top four firms in a defined product market.13The 1982 Guidelines were the first to adopt the HHI as a basis for the structural presumption. See U.S. Dep’t of Just., 1982 Merger Guidelines 12 (1982), https://perma.cc/5E63-BN59. For a discussion of the role of that presumption, see Hovenkamp & Shapiro, supra note 12. Under the 2010 Guidelines, for example, a market is highly concentrated and mergers are presumptively illegal after the market reaches a level of 2500 HHI, reflecting a market of four equally sized rivals.142010 Merger Guidelines, supra note 12, at 19. See also Bill Baer, Jonathan B. Baker, Michael Kades, Fiona Scott Morton, Nancy L. Rose, Carl Shapiro & Tim Wu, Restoring Competition in the United States: A Vision for Antitrust Enforcement for the Next Administration and Congress 27 (2020), http://perma.cc/6D9T-SCL2 (finding the 2010 Merger Guidelines “raised the market concentration thresholds for presumptively anticompetitive mergers[] to a level that focused enforcement on transactions that would leave no more than four equal-sized competitors post-merger . . . .”).

For a contrast to Von’s Grocery, consider the Court of Appeals for the Ninth Circuit’s 1990 decision in United States v. Syufy Enterprises.15903 F.2d 659 (9th Cir. 1990). That case involved movie theatres in Las Vegas.16Id. at 661. In particular, the DOJ challenged Syufy’s acquisition of competing theatres as a violation of the antitrust laws.17Id. Unlike Von’s Grocery, the Syufy court ruled against the DOJ, invoking its own merger guidelines and pointing to the absence of barriers to entry.18Id at. 664. And the Ninth Circuit drove this point home by highlighting the empirical realities of the market: “Syufy’s acquisitions did not short circuit the operation of the natural market forces; Las Vegas’ first-run film market was more competitive when this case came to trial than before Syufy bought out Mann, Plitt and Cragin.”19Id. at 665. In short, within a generation, the DOJ went from receiving every benefit of the doubt in challenging a merger to being put to the test to prove competitive harm based on economic rigor.20To be sure, there were concerns that the approach in Syufy could undermine effective merger enforcement. See Jonathan B. Baker, The Problem with Baker Hughes and Syufy: On the Role of Entry in Merger Analysis, 65 Antitrust L.J. 353, 371 (1997) (“A court that disregards the entry likelihood issue, or presumes that examples of past entry are dispositive on the issue of the profitability of future entry, may find itself wrongly allowing anticompetitive mergers to proceed.”). In practice, the implementation of the 1992 Merger Guidelines, which addressed the proper role of entry analysis, appears to have addressed that concern. See, e.g., FTC v. Cardinal Health, Inc., 12 F. Supp. 2d 34, 55–58 (D.D.C. 1998) (relying on the Guidelines in ease-of-entry analysis). Moreover, courts have generally respected the role of the so-called structural presumption, meaning mergers that move a market to a certain level of concentration are presumptively illegal. Hovenkamp & Shapiro, supra note 12, at 2013–14.

The Chicago School critique, or revolution as some have called it, recast antitrust law within a generation. The change was not only like that seen from Von’s Grocery to Syufy in the analysis of mergers between competitors (horizontal mergers), but also in the analysis of “vertical” relationships (terms of dealing between suppliers and distributors). Most notably, within a little more than a decade, the Supreme Court changed its tune on the proper mode of analyzing requirements imposed by suppliers on distributors. In Continental T.V., Inc. v. GTE Sylvania Inc.,21433 U.S. 36 (1977). the Supreme Court overruled United States v. Arnold, Schwinn & Co.,22388 U.S. 365 (1967). holding that a supplier’s imposition of terms on a distributor—in this case, retailers’ franchise territories—was no longer per se illegal, but should be analyzed under the rule of reason to determine the actual economic impact.23GTE Sylvania, 433 U.S. at 57–58.

In the context of the facts of GTE Sylvania, the ruling was a victory for economics, the Chicago School, and common sense. After all, Sylvania’s TV manufacturing business was a small part of the overall market, with around a 1% market share.24Id. at 38. In GTE Sylvania, the Court’s emphasis on interbrand competition, Sylvania’s competition with rival TV manufacturers, over intrabrand competition, rivalry between distributors who sold Sylvania TV sets, made a ton of sense. But as Justice White noted in his concurrence in the judgment, there is a potential difference in the relative competitive significance between interbrand competition versus intrabrand competition in a highly concentrated market.25Id. at 63–64 (White, J., concurring in judgment). Notably, where there is limited competition between brands, the competition within a brand—say, price cutting by discount retailers—might (without the vertical restraints) be a powerful means of benefitting consumers. The connection between market power and anticompetitive vertical restraints is discussed in Christine A. Varney, Assistant Att’y Gen., Antitrust Div., U.S. Dep’t of Just., Remarks as Prepared for the National Association of Attorneys General and Columbia Law School State Attorneys General Program, Antitrust Federalism: Enhancing Federal/State Cooperation (Oct. 7, 2009), https://perma.cc/7BV4-8FMR.

In today’s economy, skepticism towards antitrust enforcement is far less warranted than it was during Von’s Grocery (1966), GTE Sylvania (1977), or even Syufy (1990). After all, as Professor Carl Shapiro recently explained, “evidence that U.S. markets have become more concentrated, evidence that price/cost margins have risen, evidence that entry barriers have become higher, and evidence that corporate profits have risen substantially and are expected to persist” all support the need for more active merger enforcement.26Shapiro, supra note 1, at 738. Indeed, we are now a world away in terms of the level of competition from that earlier era, meaning that more vigilance is called for both in overseeing mergers and vertical integration. The next Part will discuss those challenges.

II. The Critical Role of Merger Enforcement

The role of governmental antitrust enforcement is not merely to police anticompetitive conduct, but also to set rules of the road for an administrable antitrust system. Such rules enable firms to self-police based on their understanding of the relevant boundaries, with antitrust lawyers able to counsel firms on how to do so. In principle, the Merger Guidelines provide valuable guidance in this respect. But in practice, firms push the envelope to test what actions enforcers will challenge as illegal.

Today’s cause for concern is not overly aggressive antitrust enforcement, but that increasing industry concentration is harming consumers, workers, and innovation. For a case in point, consider the airline industry. As a group of commentators summarized: “[B]etween 2005 and 2014, the [DOJ] Antitrust Division reviewed seven airline mergers. In five of those cases, there were no challenges, and the antitrust division settled the other two. Now, four airlines control almost 70 percent of domestic air travel in the United States.”27Baer et al., supra note 14, at 28. And because consumers are basically limited to the flights available from nearby local airports, most consumers, in practice, are left to choose between two or three airlines when making travel plans. There is also little to no entry in this sector, as discussed in Part III, in part because incumbent airlines have developed a reputation for predation.28See James L. Robenalt, Note, Predatory Pricing in the Low-Fare Airline Market: Targeted, Discriminatory, and Achieved with Impunity, 68 Ohio St. L.J. 641, 644 n.18 (2007). Finally, in what demonstrates the clear consumer harm from the high level of concentration in the airline industry, consumers did not see any benefits passed on to them when fuel prices fell dramatically.29See Jad Mouawad, Airlines Reap Record Profits, and Passengers Get Peanuts, N.Y. Times (Feb. 6, 2016), https://perma.cc/8EJ6-HE88. Rather, the industry recorded massive profits.30Id. (“A decade of consolidation has reduced the number of airlines competing in many markets, making it easier for dominant carriers to charge more for flights.”).

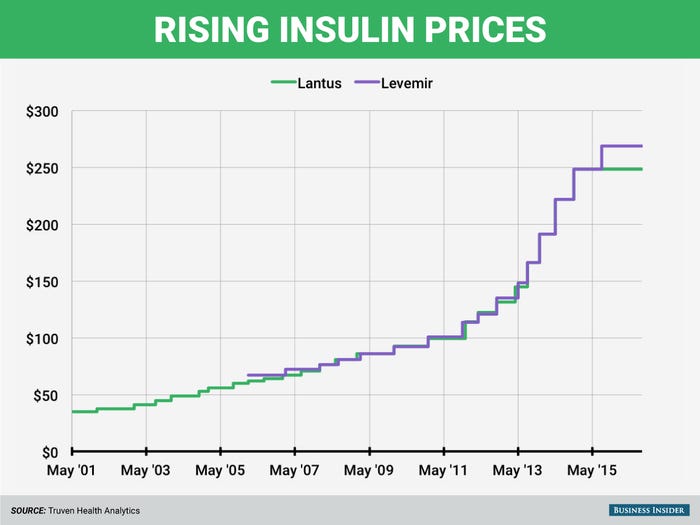

What is taking place in the airline industry is far from unique. Consider, for another example, the case of the pharmaceutical industry and the market for insulin. The State of Colorado Attorney General’s Office (“the COAG”) recently studied this market, issuing a report that analyzes why insulin prices rose so much faster than the rate of inflation and calling for action to promote competition.31Colo. Dep’t of Law, Prescription Insulin Drug Pricing Report 2–5 (2020), http://perma.cc/JS66-9R6H. The COAG found that with only three firms in the marketplace, their pricing patterns were troubling at best. Figure 1 illustrates the insulin pricing situation between two incumbent firms that mirrors the dynamic described in the COAG’s investigation.32This graph is printed in black and white, and thus modified from its original version. For an original production of the graph, see Lydia Ramsey Pflanzer, There’s Something Odd About the Way Insulin Prices Change, Bus. Insider (Sept. 17, 2016), http://perma.cc/CEQ9-M6GH.

Figure 1

What these numbers do not capture is the impact on people, especially the most vulnerable among us, such as those without health insurance who end up paying even more for insulin—a life-saving drug. In a survey of Colorado consumers, many individuals reported suffering on account of these rising insulin prices, including the more than 40% of survey respondents who are forced to ration their use of this life-saving product at least once a year.33Colo. Dep’t of Law, supra note 31, at 16. In some cases, consumers “even reported choosing to fast as a means of managing their blood sugar levels.”34Id. at 2.

In industries with few competitors, such as the pharmaceutical industry wherein three firms provide insulin, a practice of lockstep pricing or tacit collusion is both appealing and feasible. On the front end, the best strategy to prevent such a dynamic is effective merger control, preventing industries like airlines or pharmaceuticals from becoming overly concentrated.35See Shapiro, supra note 1, at 738 (“Merger enforcement is especially important since a wide range of interdependent conduct by oligopolists, i.e., conduct whereby the oligopolists refrain from vigorous competition, is not considered to be illegal if it does not involve an agreement among those oligopolists.”). On the back end, competition policy should encourage and enable entry, such as some of the patent reform measures advocated for in the COAG’s insulin report.36Colo. Dep’t of Law, supra note 31, at 54–56. And where enforcers can identify quid-pro-quo collusion—such as price fixing—it is critical that they take action, as a coalition of State Attorneys General are doing in a case against generic drug companies who have raised prices through cartel-like behavior.37Complaint, Connecticut v. Sandoz, Inc., No. 3:20-cv-00802 (D. Conn. June 10, 2020).

Finally, it bears emphasis that the increasing industry concentration can also lead to a more difficult environment for entry and innovation where dominant firms control critical inputs necessary for entry. This dynamic can be created or exacerbated by vertical mergers. As a result of such mergers, dominant firms can harm competition by gaining control over, and then restricting, access to a critical input—say, by raising the input’s price or degrading its quality. In some cases, such action can involve foreclosing a distribution channel (e.g., limiting access to sales channels); in other cases, it can involve acquiring a critical component part of a product (e.g., a cable company buying video programming).38The 2020 Vertical Merger Guidelines address both concerns. U.S. Dep’t of Just. & Fed. Trade Comm’n, Vertical Merger Guidelines 4–8 (2020), http://perma.cc/T7YV-36J2.

In the spring of 2019, the COAG confronted such a concern and took action to protect competition in the Medicare Advantage market by preventing a vertical merger between UnitedHealth and DaVita that would have impaired competition by eliminating a competitor’s access to a critical input.39Complaint at 14–15, Colorado v. UnitedHealth Grp., Inc., No. 2019CV31424 (Colo. Dist. Ct. June 19, 2019). In the years leading up to the merger, the health insurance provider Humana had entered the Medicare Advantage market in Colorado Springs and eroded the market share of UnitedHealth, the dominant firm, from around 75% to around 50%.40Id. at 16. Critical to Humana’s success in this market was its relationship with DaVita’s clinics, which referred patients to Humana’s Medicare Advantage offering—a relationship that might well have ceased in the wake of UnitedHealth’s proposed merger with DaVita. While the FTC declined to take action to address this competitive harm in Colorado, the COAG did take action, imposing a remedy that protected competition in this market with the aid of the FTC staff and the support of two FTC Commissioners.41Statement, Fed. Trade Comm’n, Statement of Commissioners Rebecca Kelly Slaughter and Rohit Chopra, In re UnitedHealth Group and DaVita, Comm’n File No. 181-0057 (June 19, 2019), https://perma.cc/JLT5-Y68R.

For another powerful case in point, and reflection of the state of our economy, consider Steves & Sons, Inc. v. Jeld-Wen, Inc.,42345 F. Supp. 3d 614 (E.D. Va. 2018), appeal dismissed, No. 19-2466, 2020 WL 3422366 (4th Cir. June 8, 2020). which involved the door manufacturing business. In 2000, this industry was robustly competitive with many door manufacturers able to operate independently and buy critical component parts, including interior molded doorskins.43Id. at 624. At that time, there were two manufacturers of this component part: Masonite and JELD-WEN. JELD-WEN, however, was vertically integrated, meaning that it both manufactured doorskins as well as used them internally to sell finished doors.44Id. at 624–25. In 2001, Masonite—including its premier manufacturing plant in Towanda, Pennsylvania—was set to be sold to Premdor, one of the then-independent door manufacturing firms.45Id. at 627. In response to concerns by independent door manufacturers, the DOJ required the divestiture of the Towanda plant from Premdor and the establishment of a new firm, Craftmaster International, Inc. (“CMI”), which would be able and motivated to sell doorskins to independent door manufacturers.46Id. And from 2002–2012, CMI did just that, continuing the status quo ante before the Masonite-Premdor merger and providing a third rival seller of molded doorskins.47Id. at 628.

In 2012, JELD-WEN expressed an interest in acquiring CMI, but before consummating the deal and approaching the DOJ, it “entered into long-term supply contracts with the Independents, knowing that this oft-used tactic would assuage the concerns of the [DOJ] and the Independents about anticompetitive effects of the proposed merger.”48Steves & Sons, 345 F. Supp. 3d at 631. JELD-WEN’s tactic was successful, as when the DOJ contacted independent firms like Steves & Sons, they expressed no concerns about the merger, citing the long-term supply agreement.49Id. Once the merger was consummated, however, JELD-WEN closed one of its existing plants and, notwithstanding declining costs, proceeded to raise prices to Steves & Sons and other independent firms under the supply agreement.50Id. at 631, 635. JELD-WEN also changed its policy on reimbursing Steves & Sons for the cost of doors rendered defective by flawed doorskins.51Id. at 636. In making these changes, JELD-WEN took advantage of its role as the only supplier of doorskins to independent door manufacturers, even sending Steves & Sons a public presentation that Masonite had made to investors stating that it would not sell doorskins to the independent firms.52Id. at 635–36.

In 2016, Steves & Sons took the unprecedented step of challenging the 2012 merger as illegal and calling for divestiture of CMI from JELD-WEN.53Id. at 640. Steves & Sons demonstrated the adverse competitive consequences outlined above and provided evidence that it was unable to meet its need for doorskins from foreign sources or establish its own source of domestic supply. Acknowledging that divestiture is the “most drastic, but most effective, of antitrust remedies[,]”54Steves & Sons, 345 F. Supp. 3d at 648 (quoting United States v. E.I. du Pont de Nemours & Co., 366 U.S. 316, 326 (1961)). the court ultimately turned to history as its guide in justifying this step:

[I]n the spring of 2012, there were three vertically integrated doorskin suppliers: Masonite, JELD-WEN; and CMI. The record shows that these three companies competed vigorously in selling doorskins to Steves and the other independent (non-integrated) door manufacturers. That is pointedly illustrated by the fact that, in 2011 and 2012, Steves was in negotiations for a new long-term supply contract, and there was significant price competition for Steves’ business.55Id. at 667.

The arc of merger law—from Von’s Grocery to Steves & Sons—captures both the value of the Chicago School critique and its overreach. To defend the merger in Steves & Sons and to oppose antitrust enforcement in cases like it is an unjustified extension of the original Chicago School critique. Stated more broadly, the central challenge for antitrust law today is not to tame over-enforcement akin to Von’s Grocery, but to address the risk of under-enforcement made plain by a case like Steves & Sons.56This balance is often framed as the costs of false positives versus the costs of false negatives. As Jonathan Baker has explained, far more attention is now needed on the impact of false negatives—that is, the failure to bring important cases. See Jonathan B. Baker, The Antitrust Paradigm 74 (2019). After all, if this private action unearthed what was clearly an anticompetitive merger, how many other such mergers have gone through and not been examined after the fact? The facts of the Steves & Sons case, along with the lack of competition in the airline and pharmaceutical industries, underscore that consumers, workers, and innovative firms are hurt when the lack of antitrust enforcement allows firms to establish and maintain market power.

III. Dominant Firms and the Role of Section 2

Over the last several decades, the Supreme Court has undermined the path for curbing the harm to competition from monopolies under section 2 of the Sherman Act by erecting a series of artificial hurdles for enforcers to meet.57Baer et al., supra note 14, at 11 (“[T]he courts increasingly saddle plaintiffs with inappropriate burdens, making it unnecessarily difficult to prove meritorious cases and allowing anticompetitive conduct to escape condemnation.” (citing Ohio v. American Express Co., 138 S. Ct. 2274 (2018) and Verizon Commc’ns, Inc. v. Trinko, 540 U.S. 398 (2004)); Carl Shapiro, Protecting Competition in the American Economy: Merger Control, Tech Titans, Labor Markets, J. Econ. Perspects., Summer 2019, at 70 (“The fundamental problem in [the standard for exclusionary conduct under Section 2 of the Sherman Act] is that the Supreme Court has, over the past 40 years, dramatically narrowed the reach of the Sherman Act.”). For one such example, consider the impact of Brooke Group Ltd. v. Brown & Williamson Tobacco Corp.,58509 U.S. 209 (1993). which addressed the law of predatory pricing.59Technically speaking, Brooke Group involved a Robinson Patman Act claim, but the Supreme Court later made clear that its analysis applied fully to the section 2 context. For a discussion of Brooke Group and its impact, see C. Scott Hemphill & Philip J. Weiser, Beyond Brooke Group: Bringing Reality to the Law of Predatory Pricing, 127 Yale L.J. 2048 (2018); see also Aaron S. Edlin, Predatory Pricing: Limiting Brooke Group to Monopolies and Sound Implementation of Price-Cost Comparisons, 127 Yale L.J. Forum 996 (2018). In Brooke Group, the Court imposed both a price-cost test (predatory pricing involves pricing below costs) and a recoupment test (meaning that a plaintiff must demonstrate a likelihood of profiting from the practice).60Brooke Group, 509 U.S. at 231–32. In so doing, the Court—quite purposefully—suggested that predatory pricing is rare and may even be implausible.61Id. at 227–28. In response, we have seen a very limited use of this doctrine over the last quarter century.

As explained earlier, the once vibrant wave of entry into the airline industry has subsided and a wave of concentration has led to market power that has hurt consumers. One of the reasons behind the lack of entry is the failure of antitrust to address predation by dominant firms. Notably, in the face of a successful effort by American Airlines to exclude a rival through predatory pricing, the Court of Appeals for the Tenth Circuit rejected the DOJ’s lawsuit.62United States v. AMR Corp., 335 F.3d 1109, 1120–21 (10th Cir. 2003). In particular, even though American Airlines ramped up capacity and reduced prices dramatically in response to the entry of a low-cost carrier, the Tenth Circuit concluded that the airline had not engaged in unlawful below-cost pricing because of how the court viewed the opportunity cost of rerouting an airplane.63Id. at 1119–20. With that unfortunate conclusion in hand, the court did not fully wrestle with, as Scott Hemphill and I put it, whether the recoupment test could be satisfied when a firm developed “a reputation for predation by its conduct in one or multiple markets, and thereby deter[ed] entry into and preserve[d] monopoly profits in other markets.”64Hemphill & Weiser, supra note 59, at 2067.

The ability of an incumbent monopolist to deter entry and competition through developing a reputation for predation has created increasing concern among economists.65For a discussion of this concern, see Patrick Bolton, Joseph F. Brodley & Michael H. Riordan, Predatory Pricing: Strategic Theory and Legal Policy, 88 Geo. L.J. 2239, 2299–310 (2000). In the recently filed case against Facebook, a coalition of states developed this very argument as a basis of section 2 liability.66Complaint at 5–7, New York v. Facebook, Inc., No. 1:20-cv-03589 (D.D.C. 2020). In short, the states argued that Facebook engaged in a campaign of threatening to “buy-or-bury” its rivals.67Id. at 6. As a result, rivals were given a choice—to be purchased in their infancy or face “the wrath of Mark [Zuckerberg],” meaning a denial of access to critical opportunities that could undermine their businesses.68Id. at 7. Facebook’s goal, in other words, was to buy upstart rivals before they emerged as serious threats or to degrade their ability to compete on the merits.

Like the Steves & Sons case, the case against Facebook involved a careful review of what happened in the wake of a consummated merger. In particular, it evaluated the impact of the “buy-or-bury” strategy and recognized that Facebook abused its monopoly power by purchasing upstart rivals—Instagram and WhatsApp in particular—to protect its dominant position in the personal social networking market.69Id. at 8–9. Consequently, the complaint alleged violations of section 7 of the Clayton Act and section 2 of the Sherman Act, asking for both divestiture relief as well as oversight of Facebook’s platform so it could not engage in discriminatory access for purposes of excluding rivals’ ability to compete on the merits.70Id. at 74–75. On June 28, 2021, U.S. District Court Judge James E. Boasberg dismissed the state enforcers’ case against Facebook. See Memorandum Opinion, New York v. Facebook, Inc., No. 1:20-cv-03589 (D.D.C. 2021).

The current case against Google likewise turns on an incumbent’s ability to exclude rivals through predation and echoes the case against Microsoft from a generation earlier. In United States v. Microsoft Corp.,71253 F.3d 34 (D.C. Cir. 2001). a unanimous D.C. Circuit concluded that Microsoft took a series of actions that excluded technologies that threatened to erode its operating system monopoly, including entering into exclusionary contracts, degrading access to its platform, and keeping barriers to entry artificially high.72See id. at 70–71, 77–79 (“[T]he question in this case is not whether Java or Navigator would actually have developed into viable platform substitutes, but (1) whether as a general matter the exclusion of nascent threats is the type of conduct that is reasonably capable of contributing significantly to a defendant’s continued monopoly power and (2) whether Java and Navigator reasonably constituted nascent threats at the time Microsoft engaged in the anticompetitive conduct at issue.”). For a discussion of the nascent threat standard, see C. Scott Hemphill & Tim Wu, Nascent Competitors, 168 U. Pa. L. Rev. 1879, 1896–903 (2020). This victory reflected the significance and importance of presenting a thorough factual analysis, proven at trial, that demonstrated how an incumbent monopolist engaged in exclusionary conduct not justified on efficiency grounds. That model applies to the Google case, which involves a series of actions taken by the company that have sought to defend and entrench its monopolies in search and search advertising, including entering into exclusionary contracts and inhibiting the ability of other companies to acquire customers of their own.73Complaint at 5, Colorado v. Google LLC, No. 1:20-cv-03715 (D.D.C. 2020). In both cases, the companies faced threats to their dominance from an adjacent sector and responded, not by competing on the merits, but by undermining the ability of rivals to compete.74See Carl Shapiro, Microsoft: A Remedial Failure, 75 Antitrust L.J. 739, 744–46 (2009) (discussing this dynamic in the Microsoft case). To remedy such conduct and restore competition requires not merely ending the illegal conduct, but “taking affirmative steps to lower the barriers to entry.”75Id. at 748.

Conclusion

We are living at a moment that calls for bold antitrust leadership. The trend in antitrust doctrine, however, is to impose unwarranted obstacles to enforcement, which is leading Congress to consider whether legislative action is necessary to remove these obstacles.76See Majority Staff of H. Subcomm. on Antitrust, Commercial and Admin. L. of the Comm. on the Judiciary, 116th Cong., Investigation of Competition in Digital Markets 6–9 (2020), https://perma.cc/UL4E-GBCR. One important role for antitrust enforcement is to recognize the power of bringing and proving cases that demonstrate clear instances of harm to competition. In that sense, the cure for the unwarranted extension of Chicago School thinking is a focus on what got the Chicago School critique started: paying attention to marketplace realities, not rigid formalities.77There is room for disagreement, of course, in describing what Chicago School adherents have in mind for the future of antitrust. Judge Posner, in discussing whether Chicago School members oppose all section 2 cases, commented that, “skepticism about unilateral monopolizing actions is not the same as denial.” Richard A. Posner, Antitrust in the New Economy, 68 Antitrust L.J. 925, 933 (2001). Professors Hovenkamp and Scott Morton are less sanguine about the openness of Chicago School adherents to such cases. See Herbert Hovenkamp & Fiona Scott Morton, Framing the Chicago School of Antitrust Analysis, 168 U. Pa. L Rev. 1843, 1847 (2020) (“Its followers were libertarians who were committed on ideological grounds to less intervention by the state.”); id. at 1848 (articulating the Chicago School principle that “markets are inherently self-correcting and if left alone, they will work themselves pure”).

To appreciate the value of a focus on marketplace realities, consider the Evanston Northwestern hospital case.78Complaint, Evanston Northwestern Healthcare Corp., Fed. Trade Comm’n Docket No. 9315 (Feb. 10, 2004), https://perma.cc/8PWT-VWLC. Before that case, the FTC had lost seven hospital merger cases in a row. As related by former–FTC Chairman Muris, some suggested that, in the face of that track record, the FTC should “give up on hospital mergers.”79Assessing Part III Administrative Litigation: Interview with Timothy J. Muris, 20 Antitrust 6, 10 (2006). Chairman Muris responded to that criticism as follows: In 2001 many said, give up on hospital mergers, but I disagreed because health care is such an important part of the economy and because there was evidence of problematic mergers. We began a retrospective study, which sounded simple, but turned out to be hard and complex. We picked several mergers, in part to bring a case or two if we found them, but also to study and report to help the government use the HSR process at some future date. Id. It declined to do so. Instead, the FTC did a series of retrospective studies, identified an already consummated merger, and demonstrated the harm to competition from a hospital merger in the Evanston Northwestern case.80Id. After a hospital merger that demonstrated a clear showing of price increases, courts have reevaluated the prior use of rigid formal tests (e.g., the misuse of the Elzinga-Hogarty patient-flow test) and have condemned other hospital mergers as anticompetitive.81See FTC v. Penn State Hershey Med. Ctr., 838 F.3d 327, 341, 353–54 (3d Cir. 2016); FTC v. Advocate Health Care Network, 841 F.3d 460, 464 (7th Cir. 2016).

Following the lessons of Evanston Northwestern, Microsoft, and Steves & Sons, the challenge for antitrust will be to demonstrate concrete factual situations that call for a reassessment of legal standards now tilted to guard against the risk of over-enforcement and undervalue the real harm caused by under-enforcement. That tilt, however, is no longer justified by current market realities.

As the new Biden Administration considers how to elevate and revitalize competition policy goals, it will have the opportunity to both reinvigorate antitrust enforcement and promote competition more broadly. As some commentators have explained, there is an opportunity for a broader assessment of how to promote competition—beyond antitrust enforcement—by establishing a new “White House Office of Competition Policy” and engaging in robust and careful studies of industries, such as in agriculture or health care, to better understand how and why competition issues arise.82Baer et al., supra note 14, at 37, 39. And at this important moment, it is crucial that antitrust commentators frame a post-Chicago School agenda for antitrust law attuned to today’s market realities.