The nirvana fallacy is the informal fallacy of comparing actual things with unrealistic, idealized alternatives. It can also refer to the tendency to assume there is a perfect solution to a particular problem. A closely related concept is the “perfect solution fallacy.”1Nirvana Fallacy, Wikipedia (citing Harold Demsetz, Information and Efficiency: Another Viewpoint, 12 J.L. & Econ. 1 (1969)), https://perma.cc/K9VY-Z9D9.

Introduction

Harold Demsetz liked to joke that he told Ronald Coase that he should have been awarded his Nobel Prize, in recognition of the fact that he, Demsetz, had published “The Problem of Social Cost” paper so many more times than had Coase.2Henry Smith, Harold Demsetz (1930-2019), New Private Law (Jan. 17, 2019), https://perma.cc/2HZS-LQ9D. It was a sharp jab thrust with Demsetzian efficiency.3Coase pondered transaction costs from the same basic perspective in many of his 1937, 1946, 1959, 1960, and 1974 works. See R. H. Coase, The Federal Communications Commission, 2 J.L. & Econ. 1 (1959); R. H. Coase, The Lighthouse in Economics, 17 J.L. & Econ. 357 (1974); R. H. Coase, The Marginal Cost Controversy, 13 Economica 169 (1946); R. H. Coase, The Nature of the Firm, 4 Economica 386 (1937); R. H. Coase, The Problem of Social Cost, 3 J.L. & Econ. 1 (1960). However, Demsetz expanded Coasian logic in papers produced in 1966, 1967, 1968, 1969, 1972, 1982, 2008, and 2011, as well as with Professor Armen Alchian in 1972. See Harold Demsetz, From Economic Man to Economic System: Essays on Human Behavior and the Institutions of Capitalism (2008) [hereinafter Demsetz, From Economic Man to Economic System]; Armen A. Alchian & Harold Demsetz, Production, Information Costs, and Economic Organizations, 62 Am. Econ. Rev. 777 (1972); Harold Demsetz, Barriers to Entry, 72 Am. Econ. Rev. 47 (1982) [hereinafter Demsetz, Barriers to Entry]; Harold Demsetz, Information and Efficiency: Another Viewpoint, 12 J.L. & Econ. 1 (1969) [hereinafter Demsetz, Information and Efficiency]; Harold Demsetz, Some Aspects of Property Law, 9 J.L. & Econ. 61 (1966); Harold Demsetz, The Cost of Transacting, 82 Q.J. Econ. 33 (1968); Harold Demsetz, The Problem of Social Cost: What Problem? A Critique of the Reasoning of A.C. Pigou and R.H. Coase, 7 Rev. L. & Econ. 1 (2011); Harold Demsetz, Toward a Theory of Property Rights, 57 Am. Econ. Rev. 347 (1967) [hereinafter Demsetz, Toward a Theory of Property Rights]; Harold Demsetz, When Does the Rule of Liability Matter?, 1 J. Legal Stud. 13 (1972); Harold Demsetz, Why Regulate Utilities?, 11 J.L. & Econ. 55 (1968) [hereinafter Demsetz, Utilities]. Of these Demsetz papers, five cite Coase in their first footnotes. In fact, Ronald Coase judged his erstwhile Chicago Law School colleague’s research to be highly impressive. Coase noted to me, at a July 1996 conference where both he and Demsetz were on the program, see generally Thomas W. Hazlett, Introduction, 41 J.L. & Econ. 521 (1998) (published papers of “Law and Economics of Property Rights to Radio Spectrum” conference), that of all the economists to grapple with his writings, Demsetz was the scholar who most deeply understood his reasoning.

But Demsetz—who went without a Nobel Prize, a Theorem, or an obituary in the New York Times—nonetheless coined a famous Critique and minted his own Fallacy. The Nirvana Fallacy is a “false dichotomy,” says Wikipedia, that “presents one option which is obviously advantageous—while at the same time being completely implausible.”4Nirvana Fallacy, supra note 1. It is a tidy, splendid adage that restates Coase’s critique of Pigouvian welfare economics in two words.

Demsetz’s prolific research agenda, including his Critique, focused on the organization of firms and the structure of markets. His body of work provides vital assistance in the policy controversies raging this day. Not for generations have public and scholarly demands for policies to deconcentrate markets been as pronounced, nor have the analytical tools of price theory been as controversial. Of great assistance is that Demsetz reasoned from well-chosen examples that became parables bursting with testable implications.5Of the many that Demsetz used, the classic demonstration is supplied by his description of native tribes in Quebec endeavoring to expand exclusive beaver habitat property rights when furs were made more valuable by the arrival of French traders. Demsetz, Toward a Theory of Property Rights, supra note 3, at 351–52. Demsetz later referenced his approach as a “literary ‘hook’ [of] an anthropological puzzle.” Demsetz, From Economic Man to Economic System, supra note 3, at 84. Demsetz uses another “literary” reference to excellent effect in that same book: “The complexities of ownership are illustrated in Herman Melville’s classic, Moby Dick.” Id. at 91. Professor Henry Smith accurately captured the gist: “Harold was never a ‘blackboard economist.’ His work was always tethered to reality.”6Smith, supra note 2.

Ironically, the reality of market rivalry that Demsetz pondered has slipped from fashion at this dirigiste moment in antitrust policy. The logical twist is the timing, coming in the wake of the “Internet Revolution,” a social transformation giving rise to protean technologies and innovative business models.7See, e.g., Internet Revolution, Encyclopedia.com, https://perma.cc/5SXH-33R4. While these have helped lift billions, dramatically reducing poverty8“Over the last 25 years, more than a billion people have lifted themselves out of extreme poverty, and the global poverty rate is now lower than it has ever been in recorded history.” Jim Yong Kim, President, World Bank Grp., Address regarding World Bank Group Poverty and Shared Prosperity Report, as quoted in Press Release, The World Bank, Decline of Global Extreme Poverty Continues But Has Slowed: World Bank (Sept. 19, 2018), https://perma.cc/3CS4-RUM8. and worldwide income inequality,9“Between 2008 and 2013, global inequality fell for the first time since the industrial revolution . . . .” Yes, Global Inequality Has Fallen. No, We Shouldn’t Be Complacent, The World Bank (Oct. 23, 2019), https://perma.cc/UW92-HVKR. emerging critiques of large software, e-commerce, and social media platforms have produced a political “Techlash.”10Rana Foroohar, The Word of the Year: Techlash, Fin. Times (Dec. 16, 2018), https://perma.cc/FKQ5-ZD5X. Antitrust scholars have launched a “new structuralism,” also known as “Hipster Antitrust,”11Joshua D. Wright, Elyse Dorsey, Jonathan Klick & Jan M. Rybnicek, Requiem for a Paradox: The Dubious Rise and Inevitable Fall of Hipster Antitrust, 51 Ariz. St. L.J. 293, 294 (2018). with its leaders, the “New Brandeisians,”12Lina Khan, The New Brandeis Movement: America’s Antimonopoly Debate, 9 J. Eur. Comp. L. & Prac. 131, 132 (2018). arguing against the utility of these industrial innovations, veering into what the New Brandeisians call “the curse of bigness.”13Tim Wu, The Curse of Bigness: Antitrust in the New Gilded Age 15–16 (2018); Jake Walter-Warner & William F. Cavanaugh, Jr., The New Brandeis School Manifesto, Patterson Belknap (Feb. 5, 2020), https://perma.cc/Z4WR-BUZF.

The purpose of this Article is twofold. First, it argues that Demsetz’s writings powerfully leverage the public policy paradigm laid out in Coase’s “The Problem of Social Cost.” While Demsetz’s extraordinary contribution to the property rights and transaction cost literature is widely appreciated,14Richard Epstein, The Greatness of Harold Demsetz, Ricochet (Jan. 14, 2019), https://perma.cc/ELU2-SMUR (“Within the legal academy, Demsetz’s most influential article . . . was entitled Toward a Theory of Property Rights. Written in 1967, it complements his work on the firm. Demsetz had no formal training as a lawyer but had a terrific eye for legal problems. This short masterpiece was perhaps the first to systematically link together changes in property rights regimes with changes in the intensity of use of a scarce resource.”). this work seamlessly applies to the antitrust policy analysis presented in Demsetz’s industrial organization research.

The second objective of this Article is to show that the Demsetzian approach to market power, through both the Nirvana Fallacy and the Demsetz Critique of the Structure-Conduct-Performance framework,15See Harold Demsetz, Industry Structure, Market Rivalry, and Public Policy, 16 J.L. & Econ. 1, 1–4 (1973) [hereinafter Demsetz, Industry Structure]; see also Joe S. Bain, Relation of Profit Rate to Industry Concentration: American Manufacturing, 1936-1940, 65 Q.J. Econ. 293 (1951). Sam Peltzman refers to Demsetz’s critique of the Structure-Conduct-Performance framework as the “Demsetz Critique.” Sam Peltzman, Sam Peltzman on Harold Demsetz, UCLA Econ. (Jan. 16, 2019), https://perma.cc/Z69B-XCLQ; see also Bain, supra; Demsetz, Industry Structure, supra, at 1–4. applies with great force to regulatory conclusions advanced today. Professor and legal scholar Richard Epstein observed that “Demsetz’s passing marks the end of an era now that . . . legal scholars Tim Wu and Lina Khan attack Chicago-style antitrust law for wrongly exalting economic efficiency over all other values . . . .”16Epstein, supra note 14. Khan, whose widely cited ninety-six-page essay in the 2017 Yale Law Journal focused on the alleged harms caused by Amazon’s success in online retailing,17Lina M. Khan, Amazon’s Antitrust Paradox, 126 Yale L.J. 710, 716–17 (2017). has recently been appointed to Chair of the Federal Trade Commission.18David McCabe & Cecilia Kang, Biden Names Lina Khan, a Big-Tech Critic, as F.T.C. Chair, N.Y. Times (June 15, 2021), https://perma.cc/C83Y-Z8U5. She sees monopoly power, predatory conduct, and vertical foreclosure endemic in the New Economy. Wu—a Columbia law professor, member of President Biden’s National Economic Council, and student of Richard Posner—adds that the “rise of the Tech Trusts” should be countered by a “[New]-Brandeisian” antitrust movement that brings “big case[s]” to break-up Facebook, Google, and Amazon.19Wu, supra note 13, at 119, 126.

Professor Peter Boettke demurs. Referencing “the near-monopoly status of Amazon, Apple and Netflix,” he observes that “the work of Demsetz is as critical to understanding the dynamics of marketplace today as it was when he first approached the study of industry structure and competitive behavior.”20Peter Boettke, Harold Demsetz (1930-2019) – A Champion of Price Theory and the Economic Way of Thinking, Coordination Problem (Jan. 8, 2019, 10:08 AM), https://perma.cc/SB3H-S8XK. Boettke nicely amplifies the point: Demsetz demonstrated that deviations from the textbook notion of the ideal perfect competition model did not necessarily prevent the price system from coordinating economic activity . . . Governance matters and context matters, both theoretically as well as empirically. This is particularly relevant at the present moment, when many within the economics profession and the public policy community are stressing the potential monopoly problems associated with the “platform economy.” Id. This Article concurs and explains how Demsetz’s thinking, combined with the facts surrounding the rise of high-technology platforms in the internet era, answers “Hipster Antitrust.”

I. Nirvana and Monopoly

Economist Kenneth J. Arrow pondered how to think about information goods and the inventions that they inspire.21See Kenneth J. Arrow, Economic Welfare and the Allocation of Resources for Invention, in The Rate and Direction of Inventive Activity: Economic and Social Factors 609, 609–10 (Nat’l Bureau of Econ. Rsch. ed., 1962). Using the theory of perfect competition as an efficiency standard, Arrow focused on inherent production problems in information markets: appropriability, indivisibility, and uncertainty.22Id. at 609. Arrow concluded that each of these factors accounted “for a failure of the competitive system to achieve an optimal resource allocation . . . in the case of invention.”23Id. at 610. Thus, for superior social results, information production and distribution must become a project of government subsidies and public allocation.24Id. at 623.

This was not casual commentary, of course. It extended A.C. Pigou’s classic welfare economics.25See generally A.C. Pigou, The Economics of Welfare (4th ed. 1962). In this, it provoked the Coasian critique of asymmetric assumptions. In response, Demsetz pounced. Arrow had constructed counterfactuals comparing rival social outcomes under distinct rules of property ownership. But Arrow had artificially frozen key variables. The perfect efficiency of atomistic, decentralized private rivalry was not a fact-based option, nor was the frictionless efficiency of a state-directed (or subsidized) information production proffered by Arrow. Demsetz preferred to consider uncomplicated alternatives because “simpler ideas are easier to test.”26Liberty Fund, Inc., A Conversation with Harold Demsetz, YouTube, at 26:40 [hereinafter Interview 2008], https://perma.cc/N8DP-D7HX. His preference leaned not to sparse theories, but to real-world stories and market data. As such, “simple tests” led to insights that overpowered cleaner, more ambitious models.

Demsetz dubbed Arrow’s approach the “Nirvana Fallacy,” asserting that it relied on “perfection by incantation” and “invok[ed] an unexamined alternative.”27Demsetz, Information and Efficiency, supra note 3, at 3. This, argued Demsetz, illustrated “common fallacies in the normative use of efficiency, stressing important and often implausible hidden assumptions . . . . For example, to reach some normative conclusions it is necessary to assume that people will respond to incentives differently from the way they are responding.”282 Harold Demsetz, Efficiency, Competition, and Policy: The Organization of Economic Activity 1 (1989).

Arrow considered challenges posed by appropriability, indivisibility, and uncertainty, but undercut that dose of reality by injecting a categorical response, pronouncing decentralized, non-governmental solutions as “nonoptimal allocation of resources.”29See Arrow, supra note 21, at 616–17, 619. Demsetz saw this as a mixing of metaphors. The realism of the challenge is met with an assumption of a zero-cost policy remedy. Demsetz countered: “The nirvana approach is much more susceptible than is the comparative institution approach to committing three logical fallacies—the grass is always greener fallacy, the fallacy of the free lunch, and the people could be different fallacy.”30Demsetz, Information and Efficiency, supra note 3, at 2. Arrow had constructed a counterfactual that was nonfactual. Demsetz urged a different analysis.

A. Industrial Organization

The Nirvana Fallacy appeared to flow from the property-rights and transaction-costs literature to questions of market power. But I suspect that the logical trend might have been the reverse. That is because the fallacies cited, which go to the centrality of the ceteris paribus assumption, are distinctly embedded in the industrial organization of economist Joseph Schumpeter.

Capturing gains from costs sunk in the pursuit of innovative betterment is necessarily an enterprise of something other than perfect competition. Abnormal profits lure imagination and risk-taking, where entrepreneurs address the problems of “indivisibilit[y], appropriability, and uncertainty.”31See Arrow, supra note 21, at 609–10. Confronting these challenges has become a major theme in the business strategy literature since at least 1986. See David J. Teece, Profiting from Technological Innovation: Implications for Integration, Collaboration, Licensing and Public Policy, 15 Rsch. Pol’y 285 (1986). Schumpeter distinguished the entrepreneurial function from the output optimization hypothesized in perfect competition, and—in endorsing the growth prospects of the former—undercut the presumption that “perfect” was the ideal:

[E]ntrepreneurs’ gains will practically always bear some relation to monopolistic pricing. Whatever it is that produces these gains, it must of necessity be something that, for the moment at least, competitors cannot parallel for, if they did, no surplus over costs (including entrepreneurial “wages”) could emerge. The successful introduction of a new commodity or brand is perhaps the best illustration of this.32Joseph A. Schumpeter, History of Economic Analysis 897–98 (1954). A more common reference to Schumpeter’s thinking is from his 1942 tome, Capitalism, Socialism and Democracy. There he writes: [T]here is no point in appraising the performance of that process ex visu of a given point of time; we must judge its performance over time, as it unfolds through decades or centuries. A system—any system, economic or other—that at every given point of time fully utilizes its possibilities to the best advantage may yet in the long run be inferior to a system that does so at no point of time, because the latter’s failure to do so may be a condition for the level or speed of long-run performance. Joseph A. Schumpeter, Capitalism, Socialism and Democracy 83 (Routledge 2006) (1942) [hereinafter Schumpeter, Capitalism] (emphasis omitted).

Schumpeter emphasizes that all cannot be otherwise equal across the hypothetical worlds of perfect competition’s marginal cost pricing and rivalrous innovation. Conditions associated with the latter characterize the rise of “big business” in the industrial revolution and its aftermath, as well as today’s emergent “platform industries.”33E.g., Jack High, Economic Theory and the Rise of Big Business in America, 1870-1910, 85 Bus. Hist. Rev. 85, 88 (2011) (noting that “technological innovations enabled firms to lower average variable costs by investing in large-scale plants . . . resulting [in] large-scale production, distribution, and purchasing”). See generally Peter C. Evans & Annabelle Gawer, The Rise of the Platform Enterprise: A Global Survey (2016). Neoclassical price theory was often critical of—indeed, hostile to—the efficiencies Schumpeter saw as fundamental to technological progress and rising living standards, preferring to focus on equilibrium models.34E.g., Richard R. Nelson & Sidney G. Winter, Neoclassical vs. Evolutionary Theories of Economic Growth: Critique and Prospectus, 84 Econ. J. 886, 890 (1974) (“The core ideas of Schumpeterian theory are of course quite different from those of neoclassical theory.”). Referencing conventional price theorists, he wrote: “They accept the data of the momentary situation as if there were no past or future to it . . .”35Schumpeter, Capitalism, supra note 32, at 84.

Demsetz also rejected the approach of conventional price theorists, writing that “we have no theory that allows us to deduce from the observable degree of concentration in a particular market whether or not price and output are competitive.”36Demsetz, Utilities, supra note 3, at 59–60. In his article, “Why Regulate Utilities?,” Demsetz again employed the Nirvana framework. While “sole sourced” utilities were productively efficient, price theory texts argued that public intervention to constrain the resulting monopoly prices would be unambiguously welfare-enhancing.37See id. at 56 (citation omitted). Demsetz exposed the policy error. First, the success of any rate regulation scheme, as against an unregulated (or differently treated) market, is an empirical question.38See id. at 63, 65. Moreover, there are, in fact, an infinite number of regimes that might be attempted to reform, or replace, the standard public utility rate regulation model. Second, an alternative form of policy intervention could easily be imagined, as it had been implemented in various jurisdictions: competitive bidding for the franchise.39See id. at 58–61. Were potential “monopolists” to offer long-term retail price commitments, market forces might play a much larger, and highly useful, role. Market structure need not dictate the competitive outcome. Alternatives, most basically, were to be judged on the basis of performance rather than “false dichotomies.”40See Demsetz, Information and Efficiency, supra note 3, at 1 (introducing the Nirvana Fallacy as it pertains to public policy economics).

This symmetry led Demsetz to seek evidence on the causality assumed in the Structure-Conduct-Performance (“S-C-P”) paradigm. How to test the proposition that high market share produced anticompetitive market power and, therefore, anti-consumer results? The alternative hypothesis was that competitive superiority was driving some firms to offer lower quality-adjusted prices, outcompeting rivals in attracting market share and garnering greater profits. This became known as the “Demsetz Critique.”

The correlation between market concentration and profits had been shown to be positive. Thus, the conclusion claimed by champions of the S-C-P paradigm was that the higher concentration levels were driving the higher profits, and that monopolistic output restrictions in the concentrated industries were thus revealed.41See Joe S. Bain, Industrial Organization (2d. ed. 1968), 372–468. Demsetz allowed as how that might be the case, but also that the concentration-profits correlation might be spurious.42Demsetz, Industry Structure, supra note 15, at 1–3. That is, the rise of more efficient firms, with lower costs and/or enhanced products, might logically exhibit higher growth, increasing industry concentration. In that case, the same concentration-profits correlation would be observed, but would best be explained by efficiency, not monopoly.43Id.; cf. Demsetz, Industry Structure, supra note 15, at 5 (noting that comparing industry rate of return with concentration will not distinguish rates of return as a result of efficiency versus rates of return from monopoly power).

To test his theory, Demsetz examined profit levels across firms of different sizes in markets of given concentration.44See Demsetz, Industry Structure, supra note 15, at 5–9. If high concentration were driving high profits, through collusion or output restrictions, then firms of all sizes would tend to experience high profits. Yet if high concentration was related to economies of scale, then larger firms would exhibit higher profits than smaller rival firms. This latter relationship is what the data tended to show. Demsetz concluded:

If rivals seek better ways to satisfy buyers or to produce a product, and if one or a few succeed in such endeavors, then the reward for their entrepreneurial efforts is likely to be some (short term) monopoly power and this may be associated with increased industrial concentration. To destroy such power when it arises may very well remove the incentive for progress.45Id. at 3.

The evidence was powerful, and Demsetz’s insight held up when tested by others.46See, e.g., Michael Smirlock, Thomas Gilligan & William Marshall, Tobin’s Q and the Structure-Performance Relationship, 74 Am. Econ. Rev. 1051 (1984).

Professor Ken Lehn explains, “Harold asked a very simple but penetrating question: How did the monopolist become the monopolist?”47Interview 2008, supra note 26, at 59:20. Demsetz explained that he sought to go farther upstream to discover what accounted for the rise in industrial scale that pushed market concentration up.48See id. at 17:30. By itself, initiating the conversation with the concentration-profits correlation is like telling the story by starting in the middle.49Under the S-C-P paradigm, economists “accept the data of the momentary situation as if there were no past or future to it and think that they have understood what there is to understand if they interpret the behavior of those firms by means of the principle of maximizing profits with reference to those data.” Schumpeter, Capitalism, supra note 32, at 84. More fundamentally, the notion that concentration was an independent driver of economic activity implicitly embedded the view that the capabilities of firms in the observed marketplace could be duplicated enterprises and redefined without the same scale or structure. “The trouble with theorists and with Nirvanists is they think you can create a perfect world,” said Demsetz, but “you can’t.”50Interview 2008, supra note 26, at 1:02:03. And in so attempting, they may miss the margins that do not align.

The idea for the Demsetz Critique came from faculty chitchat at the University of Chicago’s Quadrangle Club. Harold heard someone mention: “in the automobile industry the only company that’s really making money is GM.”51Id. at 15:00. From there, Harold’s investigation confirmed a revealing pattern, and he concluded that what analysts were seeing was not concentration producing market power, but “concentration through competition.”52Demsetz, Industry Structure, supra note 15, at 1. Demsetz’s research changed thinking in industrial organization. The “reflexive antipathy towards even moderate concentration levels foundered in the 1970s,” wrote Professors Tim Muris and Jonathan Neuchterlein, “on the empirical evidence and, in particular, on the highly influential research of Harold Demsetz.”53Timothy J. Muris & Jonathan E. Nuechterlein, Antitrust in the Internet Era: The Legacy of United States v. A&P, 54 Rev. Indus. Org. 651, 677 (2019). By the turn of the century, leading industrial organization texts noted that “the barrage of criticism [of the S-C-P paradigm] has caused most research in this area to cease.”54Dennis W. Carlton & Jeffrey M. Perloff, Modern Industrial Organization 268 (4th ed. 2004); see also Jeffery M. Perloff, Larry S. Karp, & Amos Golan, Estimating Market Power and Strategies (2007).

Not only did scholars move towards the Schumpeter-Demsetz approach, but public policy as well. Muris and Nuechterlein cite Demsetz’s work as the key intellectual factor motivating antitrust reforms.55See Muris & Nuechterlein, supra note 53, at 677. They write: “A concise summary of the changing views on concentration can be seen in successive editions of the Horizontal Merger Guidelines published by U.S. antitrust agencies in 1968, 1982, and 2010. In those three editions, the marginal case has effectively moved from ‘8-to-7’ mergers to 6-to-5 to 4-to-3.”56Id.

II. Brandeis Meets Demsetz

But there is no end to history. Today, the Demsetzian contribution must be learned anew. The current ascendancy in antitrust policy, colored by tinges of political populism,57Senator Elizabeth Warren (D-MA) calls for legal action to break-up Apple, Amazon, Facebook, and Google, while levying a wide range of additional regulatory and antitrust constraints on Big Tech firms. Nilay Patel, Elizabeth Warren Wants to Break Up Apple, Too: ‘Either They Run the Platform or They Play in the Store,’ The Verge (Mar. 9, 2019, 6:19 PM), https://perma.cc/8Y3S-LL4G. Meanwhile, former-President Donald Trump called for increasing regulatory oversight of, in particular, Amazon. Berkeley Lovelace Jr., Trump Says Administration Is Looking into Antitrust Violations by Amazon, Other Tech Giants, CNBC (Nov. 5, 2018, 2:20 PM), https://perma.cc/5W6V-HH23. challenges the halo so recently glimmering in the sunny skies of Silicon Valley. It also seeks to upend what it characterizes as Chicago-school thinking on industrial organization analysis and antitrust policy.

Khan’s 2017 Yale Law Journal article, “The Amazon Antitrust Paradox,” has become a sacred text58See David Streitfeld, Amazon’s Antitrust Antagonist Has a Breakthrough Idea, N.Y. Times (Sept. 7, 2018), https://perma.cc/99VN-YK96 (“With a single scholarly article, Lina Khan, 29, has reframed decades of monopoly law.”). of New-Brandeisian thinking.59See generally Khan, supra note 12. Khan emphasizes the movement’s bipartisan political support: “[T]he ‘New Brandeis School’ gains prominence—even prompting two floor speeches by Senator Orrin Hatch (a Republican from Utah) . . . .” Id. at 131. Her work borrows from the writings of Louis Brandeis, antitrust attorney, author of the Federal Trade Commission Act of 1914, and US Supreme Court Associate Justice from 1916 to 1939.60See Louis Brandeis, Britannica.com, https://perma.cc/M2UW-58FJ. As described by Thomas McCraw, Brandeis was a tireless champion of the “small dealers and worthy men”61United States v. Trans-Missouri Freight Ass’n, 166 U.S. 290, 323 (1987). that were economically threatened by large, nationally integrated enterprises arising out of the Industrial Revolution.62See Thomas McCraw, Prophets of Regulation 82 (1984). Brandeis, a brilliant polemicist, warned that “[t]he moment you allow the cutting of prices you are inviting the great, powerful men to get control . . . . Big business is not more efficient than little business.”63Id. at 104 (citation omitted). He openly opposed consumers’ economic interests, endorsing policy interventions to raise prices. When he testified in Congress favoring a ban on volume discounts, Congressman Alben Barkley (D-KY) “could not believe he had heard Brandeis correctly.”64Id. He had.

Khan crafts her Brandeisian argument to address the rise of a contemporary corporate giant, Amazon, countering Robert Bork’s Antitrust Paradox65Robert H. Bork, The Antitrust Paradox: A Policy at War with Itself (1978). with one of her own: Amazon delivers low prices and popular services but is bad for society.66See Khan, supra note 17. She argues that antitrust policy has been stripped of its protective function by Bork and influential Chicago-school economists, leaving the marketplace open for Amazon to exploit.67See id. at 780. While she fails to discuss Demsetz’s work in either her 2017 article (96 pages)68See generally id. or her 2019 article (125 pages),69See generally Lina Khan, The Separation of Platforms and Commerce, 119 Colum. L. Rev. 973 (2019). Demsetzian analysis keenly anticipates her arguments—as noted by Epstein and Boettke.70See Boettke, supra note 20 and accompanying text; Epstein, supra note 14. A virtual debate has joined Khan’s argument that the tech economy favors dangerously large-scale operations that invites widespread integration, leading to the endemic foreclosure of innovation.

A. Scale Economies

“Amazon now captures 46% of online shopping,” notes Khan, but “barely ekes out a profit.”71Khan, supra note 17, at 712–13. Where does the money go? “The company . . . spends a fortune on expansion and free shipping . . . .”72Id. at 713. This is a problem because “Amazon has established itself as an essential part of the internet economy . . . [and] its sheer scale and breadth [] may pose hazards.”73Id. at 715. Amazon has pursued a strategy of ruthless growth in sales volume, as “the premise of [its] business model was to establish scale. . . . Under this approach, aggressive investing would be key, even if that involved slashing prices or spending billions on expanding capacity, in order to become consumers’ one-stop-shop.”74Id. at 749.

The scale economies idea employed by Amazon was not new,75See Demsetz, Industry Structure, supra note 15, at 4 n.2. and Demsetz added to it by focusing attention on transaction efficiencies often related to scale. In particular, Demsetz saw consumer information as an essential production input.76See Harold Demsetz, The Effect of Consumer Experience on Brand Loyalty and the Structure of Market Demand, 30 Econometrica 22, 22 (1962). Reducing frictions in the retail experience, pioneering digital tools in burgeoning e-commerce options, Amazon has pioneered what Schumpeter called “new forms of [] organization.”77Schumpeter, Capitalism, supra note 32, at 82–83. Demsetz saw product differentiation as a component of competition, and advertising as an informational device attendant to the competitive process.78See Demsetz, supra note 76, at 22.

The idea of Amazon (or, as it was first dubbed, “Cadabra”), was concocted by a young hedge fund “quant” assigned the task, in 1994,79Brad Stone, The Everything Store: Jeff Bezos and the Age of Amazon 23–24 (2013). of determining what new business could make a profit using the emerging internet. Jeff Bezos, who landed on a plan for “an everything store,” then left his financial position at D.E. Shaw to execute his vision.80Id. at 28. He began with online book sales for three basic reasons. First, books were a commodity in the sense that, when the seller offered a title, buyers understood what they were purchasing.81Id. at 25–26. Second, there were over three million books in print, but brick-and-mortar bookstores could stock only a few thousand.82See id. at 26. This anticipated the “long tail” of web commerce.83See id. at 26, 38; see also Long Tail, Investopedia, https://perma.cc/743T-98B5. Third, while overnight delivery services had been introduced, existing book shipping—as tested by Bezos— appeared to be a mess; dramatic improvements were readily imagined.84Stone, supra note 79, at 26. Entrepreneurial action is often associated with the exploit of unarticulated knowledge, but the enterprise of Amazon was explicitly motivated by the capture of newly available efficiencies in information and transportation markets.

Once online book sales established proof of concept, Bezos pursued new product markets to share the platform, amortizing fixed costs across additional economic activity.85Cf id. at 67. Watches sold profitably, but other jewelry (particularly engagement rings, which customers like to physically inspect before purchasing) experienced more modest sales.86See id. at 184. Expanding inventories was costly and produced operating losses, as did the policy to establish “everyday low prices” (a concept borrowed from Walmart and other successful volume retailers) with generous return policies.87See id. at 125–26. These investments were made to provide customers with retail brand information, reducing customer search costs.

As Amazon’s model succeeded and grew, the platform attracted the ire of the New Brandeisians. The scale was seen to convey market dominance; the benefits in lower unit costs asymmetrically dismissed by Amazon’s critics.88See Khan, supra note 17, at 746–47. But the Amazon strategy was clear: Amazon substituted economies of scale in multiple dimensions for advertising and marketing campaigns, as well as for physical retail stores—innovations made possible by the rise of the mass-market internet.89See generally Shane Greenstein, How the Internet Became Commercial: Innovation, Privatization, and the Birth of a New Network (2015); Stan J. Liebowitz, Re-Thinking the Network Economy: The True Forces That Drive the Digital Marketplace (2002). Amazon’s model has been to offer easy online access, a user-friendly search engine, expeditious delivery service, and price guarantees as a substitute for alternative shopping options.

Amazon’s aggressive strategy to attain scale appears as unfair competition to Khan, who characterizes Amazon’s strategy as a “willingness to forego profits to establish dominance.”90Khan, supra note 17, at 747. Demsetz had framed a response to this critique thirty-five years earlier, when he wrote that: a narrow view of entry barriers that “tends to treat as unproductive the costs that must be incurred to create and to maintain a good reputation, to bear risks of innovation, and to build a scale of operations appropriate to the economical servicing of consumer demands . . . .”91Demsetz, Barriers to Entry, supra note 3, at 56.

In failing to understand the efficiencies created, or the counterfactuals, spontaneous progress is not only underappreciated but actively deterred—as with categorical limits on size or policies to impose divestitures.92See, e.g., Wu, supra note 13; Khan, supra note 69. Demsetz warns that “deconcentration may have the total effect of promoting inefficiency even though it also may reduce some monopoly caused inefficiencies.”93Demsetz, Industry Structure, supra note 15, at 4. Imposing policies that establish or mandate certain market structures—as proposed by the New Brandeisians —is dangerous work. And it misses the point. “[The] maximization of competition is a meaningless goal. The goal is more correctly described as choosing a preferred mixture of competitive forms. Thus, price competition between existing goods can be intensified by eliminating patent and copyright protection, but this reduces the effectiveness of competition to produce new goods.”94Harold Demsetz, How Many Cheers for Antitrust’s 100 Years?, 30 Econ. Inquiry 207, 207 (1992).

A Demsetzian inquiry would examine competition for the market—perhaps winner-take-all, perhaps not, cycling through changing market structures over time. That would bring into focus the differentiated strategies of eBay, Walmart, Sears, Shopify, Etsy, Google, Target, Circuit City, Best Buy, Instacart, and other rivals, some living and some dead. Barnes & Noble (“B&N”) was an established incumbent in retail book sales when Amazon was created as an online book vendor in 1995. It threatened to “launch a website soon and crush Amazon” in 1996 when the Amazon upstart had $16 million in sales and the store-based bookseller some $2 billion.95Stone, supra note 79, at 56. The B&N CEO wanted to call the new website “Book Predator” (a suggestion that was overruled), but it took months for B&N to construct a counterattack.96Id. at 57. “[D]uring that time, Bezos’s team accelerated the pace of innovation and expansion.”97Id. Out of this two-way contest emerged the tiny upstart, Amazon.98B&N, after closing most of its stores, was sold for $638 million to a hedge fund in 2019. Jordan Crucchiola, Barnes & Noble’s Wild Ride: A Timeline, Vulture (June 10, 2019), https://perma.cc/4GKM-9CX5.

Amazon’s success was not due to a predatory strategy of lowering prices in the short-term so as (after vanquishing rivals) raising prices to customers in the long run. Rather, it was guilty, as accused by the New Brandeisians, of making investments in brand awareness like this:

As if to prove his singular obsession with customer experience, Bezos placed an expensive bet . . . . In July [2000], author J.K. Rowling published the fourth book in the [Harry Potter] series, Harry Potter and the Goblet of Fire. Amazon offered a 40 percent discount on the book and express delivery so customers would get it on Saturday, July 8—the day the book was released—for the cost of regular delivery. Amazon lost a few dollars on each of about 255,000 orders, just the kind of money-losing gambit that frustrated Wall Street. But Bezos refused to see it as anything other than a move to build customer loyalty.99Stone, supra note 79, at 111. Khan identifies a much larger investment, in Amazon Prime, as presumptively predatory: As with its other ventures, Amazon lost money on Prime to gain buy-in. In 2011 it was estimated that each Prime subscriber cost Amazon at least $90 a year—$55 in shipping, $35 in digital video—and that the company therefore took an $11 loss annually for each customer. One Amazon expert tallies that Amazon has been losing $1 billion to $2 billion a year on Prime memberships. The full cost of Amazon Prime is steeper yet, given that the company has been investing heavily in warehouses, delivery facilities, and trucks, as part of its plan to speed up delivery for Prime customers—expenditures that regularly push it into the red. Khan, supra note 17, at 750. Prime was soon a “huge success,” generating great profit, after initially being very controversial within the company—precisely because it was difficult to create and expensive to build. Stone, supra note 79, at 188.

Amazon’s strategy of “get big fast” required just such outlays.100Stone, supra note 79, at 55. The end of these efforts was to create widely shared facilities: (1) inventories leveraging volume discounts; (2) delivery networks supplying quicker service than rivals; (3) easy-to-negotiate software interfaces; (4) superior customer service; and (5) “big data” to assist customers in product search and to reduce shipping and handling costs.101See, e.g., Palak Jain, How Data Science Has Helped Amazon To Be The World’s PRIME, Medium (May 21, 2019), https://perma.cc/CRJ4-ZCYA.

Khan condemns the competitive effort required to generate these objectives: “Through 2013, Amazon had generated a positive net income in just over half of its financial reporting quarters. Even in quarters in which it did enter the black, its margins were razor-thin, despite astounding growth.”102Khan, supra note 17, at 747. Short of Nirvana, is there a better option? If there were, Amazon would have been incentivized to find it. Although, by ignoring the supply-side contribution of price information, some are tempted to conclude otherwise. As Demsetz wrote: “If in some situations information is more costly or less valuable to gather, then less of it will be secured; similarly, the more costly it is to duplicate the efforts of others, the smaller will be the elasticities of the demand curves facing innovative firms.”103Harold Demsetz, Economics as a Guide to Antitrust Regulation, 19 J.L. & Econ. 371, 374 (1976). This is just where Amazon has chosen to play.

B. Vertical and Horizontal Foreclosure

Khan writes, “My argument is that gauging real competition in the twenty-first century marketplace—especially in the case of online platforms—requires analyzing the underlying structure and dynamics of markets.”104Khan, supra note 17, at 717. That is undoubtedly true, as new science and business models impact property rights, demands, and market structures. But the basic strategic issues governing entrepreneurial behavior and market efficiencies are remarkably stable. That is why we look to history to learn—even if it tempts some to reprise the policy constructs of Brandeis.

Take the launch of Amazon Web Services (“AWS”), also known as “the cloud.” This vertical extension of the Amazon e-commerce platform began in 2006, offering firms and individuals access to high-capacity data storage, retrieval, and processing services.105Stone, supra note 79, at 220; Nik Cubrilovic, Almost Exclusive: Amazon Readies Utility Computing Service, TechCrunch (Aug. 24, 2006, 9:24 AM), https://perma.cc/E35S-7ADN. It is has proven highly profitable, and AWS is now seen by financial analysts as comprising roughly one-half of total Amazon capital value.106Trefis Team, How Much Is Amazon Web Services Worth on a Standalone Basis?, Forbes (Feb. 28 2019, 3:45 PM), https://perma.cc/84KJ-NNHU. Amazon CEO Bezos believed that Amazon enjoyed “a natural advantage in its cost structure and ability to survive in the thin atmosphere of low-margin businesses,” like the cloud.107Stone, supra note 79, at 221. In 2019, Amazon accounted for 47% of global cloud revenues, with Microsoft Azure at 22%, Alibaba at 8%, and Google at 7%.108Jay Chapel, AWS vs Azure vs Google Cloud Market Share 2019: What the Latest Data Shows, Jay Chapel (July 12, 2019), https://perma.cc/SGH5-UMTV (referencing a market report conducted by Goldman Sachs).

The argument made by New- Brandeisians is that economies of scale mask anticompetitive strategies designed to exclude innovative rivals.109See Wu, supra note 13, at 68–73. This foreclosure sacrifices social growth.110See generally, Patrick Rey & Jean Tirole, A Primer on Foreclosure, in 3 Handbook of Industrial Organization 2145–220 (Mark Armstrong & Rob Porter eds., 2007). As a result, various forms of regulation, including restrictions on size (perhaps via antitrust divestiture orders), bans on mergers and acquisitions, or public utility mandates to regulate prices and terms of access (for rival suppliers as well as end users) are recommended. But how did, in fact, the cloud market arise? And how does it accommodate, or suppress, competitive forces?

First, the market was created by profit-seeking businesses, most notably Amazon. The platform could, theoretically, have been constructed by any other firm, government, or non-profit enterprise. Second, integrating cloud services with major Information Technology suppliers has, evidently, proven efficient, implying the existence of strong economies of scope. The cloud market has proven a launch pad for widely distributed, diverse enterprises. Third, pricing strategies to garner market share have encouraged rapid adoption of cloud services; Bezos reportedly demanded AWS prices be slashed 33% early on, aggressively imposing penetration pricing.111Stone, supra note 79, at 221. Fourth, the platform created serves to reduce barriers to entry in the economy generally, which Bezos characterized in an interesting historical reference:

The best analogy that I know is the electric grid. If you go back in time a hundred years, if you wanted to have electricity, you had to build your own little electric power plant, and a lot of factories did this. . . . [A]s soon as the electric power grid came online, they dumped their electric power generator, and they started buying power off of the grid. It just makes more sense. And that’s what’s starting to happen with infrastructure computing.112Jeff Bezos Talks about Amazon’s Business Model, the Popularity of the Kindle, What’s New about the Kindle 2, and Cloud Computing, Charlie Rose (Feb. 26, 2009), https://perma.cc/7Q3U-WBM6.

The vision that a global data network could be a utility, unregulated and rivalrous, is perfectly consistent with the notion that the cloud network is a grid that empowers start-ups lacking scale. Small enterprises can then plug in, buying the computation capacity they desire, capturing the gains from the economies of scale established by Amazon (or one of its cloud competitors). Constraining Amazon’s vertical extension, or blocking its growth to scale, might directly execute a Brandeisian objective, but undermine goals elsewhere, by deterring economies available to small businesses.

Khan sees Amazon as a platform creator enmeshed in a labyrinth of conflict. As economists, she argues, we have been distracted by focusing on “price and output” and have failed to see the dangers in “anticompetitive conflicts of interest.”113Khan, supra note 17, at 716–17. She posits that Amazon, as a platform provider, ensnares its customers by ostensibly cooperating at one level but then sabotaging that collaboration. In hosting third-party vendors to sell products on Amazon, for instance, Amazon monitors product sales and observes prices charged and uses the “insights gleaned from its vast Web store to build a private-label juggernaut.”114Id. at 781–82 (quoting Spencer Soper, Got a Hot Seller on Amazon? Prepare for E-Tailer to Make One Too, Bloomberg (Apr. 12, 2016, 11:00 AM), https://perma.cc/79GL-5A8E). Overall, “Amazon seeks to cut out the independent seller[].”115Id.

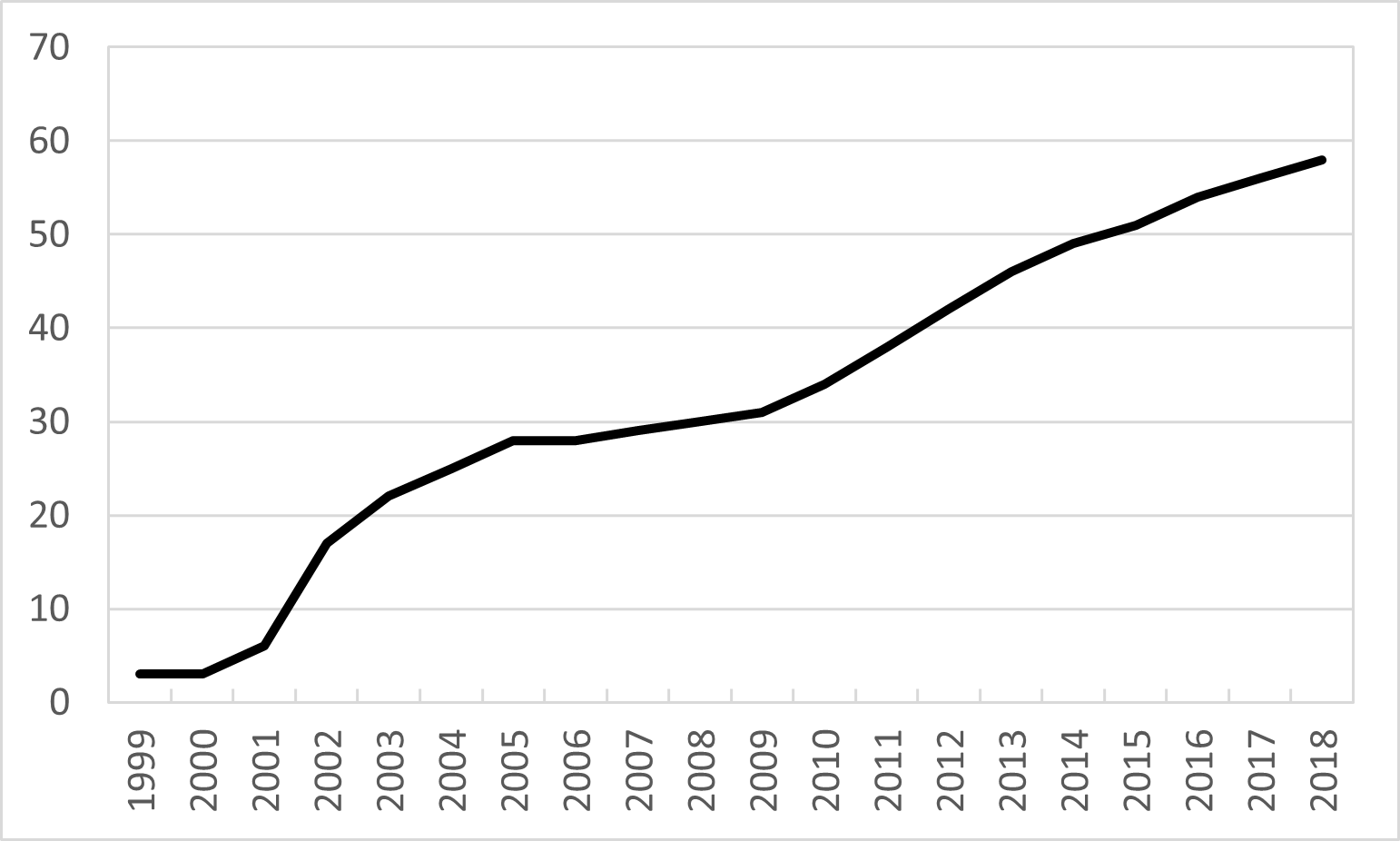

Perhaps that strategy might be efficient, as vertical integration has been generally found to deliver net consumer benefits.116See Francine Lafontaine & Margaret Slade, Vertical Integration and Firm Boundaries: The Evidence, 45 J. Econ. Literature 629, 680 (2007). But Khan’s asserted vertical integration is itself contradicted by the facts. As shown in Figure 1, in 1997, the year the company issued its Initial Public Offering, 97% of the product sales on the Amazon website were supplied by Amazon itself; by 2018 that number had declined to just 42%.

Figure 1: Percent of Amazon Gross Platform Sales by Non-Amazon Sellers117Daniel Keyes, 3rd-Party Sellers Are Thriving on Amazon, Bus. Insider (May 13, 2019, 9:44 AM), https://perma.cc/64C5-PD45.

The intervening trend was virtually monotonically in decline. Rather than stealing lucrative markets from retail vendors, Amazon has grown large by building a platform hosting independent vendors who, in turn, patronize the Fulfillment-by-Amazon because of the thick customer base attracted by the brand-name investments of Amazon. Amazon profits from this trade volume, earning about one-quarter of gross third-party sales via commissions and services (including shipping), some $40 billion in revenues in 2018.118Amazon Gross Merchandise Volume $277 Billion in 2018, Marketplace Pulse (Apr. 12, 2019), https://perma.cc/5FAR-7FTZ.

These facts do not impress the New Brandeisians. Instead, Khan focuses on “several examples of Amazon’s conduct that illustrate how the firm has established structural dominance,”119Khan, supra note 17, at 756. purporting to report Amazon’s ability and willingness to impose barriers to entry for rivals. One episode concerns the Kindle, Amazon’s e-book reader. While foreclosure is alleged, the issue is moot as the market for e-book readers (far beyond Amazon) has failed to materialize.120See Constance Grady, The 2010s Were Supposed To Bring the eBook Revolution. It Never Quite Came., Vox (Dec. 23, 2019, 10:00 AM), https://perma.cc/PB5Z-VVVC. Here I focus on the lesser-known tales of Diapers.com and Pillow Pets. These concern small third-party sellers on Amazon who were allegedly extinguished by their e-commerce landlord, Amazon, which acquired and appropriated the sellers’ market intelligence for its own benefit, rendering the sellers asunder.

Were such experiences the norm, it would be curious why Amazon was developing such an increasingly popular sales service for third-party vendors. Indeed, the reality is that both stories, appropriately sketched, strongly support the empirical observation that Amazon creates value for third-party vendors. It bears noting that Amazon’s business model competes directly with eBay, a firm that, in 2005, enjoyed three times the market capitalization of Amazon.121Stone, supra note 79, at 194. eBay is a “pure” reseller, auctioning only merchandise sold by independent firms, and hence avoids the incentive conflicts asserted to undercut Amazon’s efficiency.122Akshat Bansal, How eBay Works: Business & Revenue Model, Jungleworks (May 3, 2018), https://perma.cc/A6T8-S8LZ. Yet, by the revealed preferences of independent third-party sellers, Amazon is the preferred option. It accounts for twice the annual gross merchandise volume as eBay, counting only non-Amazon vendors, today.123Amazon GMV in 2019, Marketplace Pulse (Feb. 4, 2020), https://perma.cc/64VY-3V8Y (reporting an annual Amazon gross merchandise volume (“GMV”) from third-party sellers of $200 billion); Natalie Gagliordi, eBay Beats Q4 Expectations, GMV Down 5%: eBay Said Gross Merchandise Volume Was Down 5% Year Over Year to $23.3 Billion, ZDNet: Between the Lines (Jan. 28, 2020, 21:52 GMT), https://perma.cc/43EH-TVQZ (reporting a quarterly GMV of $23.3 billion).

In a clear application of the Nirvana Fallacy, Khan notes how Fulfilment-by-Amazon supports third-party sellers but calls it an effort to “harness the weakness of its rivals into a business opportunity.”124Khan, supra note 17, at 776. To Khan, Amazon’s supply of logistics, shipping (including fast Amazon Prime service), and customer service is but a partly friendly gesture: “Since many merchants selling on Amazon are competing with Amazon’s own retail operation and its Amazon Prime service, using FBA offers sellers the opportunity to compete at less of a disadvantage.”125Id. However, “Amazon’s conduct suggests that psychological intimidation can discourage new entry that would challenge a dominant player’s market power.”126Id. at 768.

C. Diapers.com

Quidsi was founded by two young New Jersey entrepreneurs, Marc Lore and Vinit Bharara, in 2005.127Stone, supra note 79, at 295. Their best-selling baby products were marketed on their website, Diapers.com.128Id. By “2008, Quidsi was one of the world’s fastest growing e-commerce companies.”129Khan, supra note 17, at 768. It used the Amazon e-commerce platform, which allowed Amazon to monitor the situation with its “pricing bots.”130Id. at 769. Amazon subsequently integrated into diaper sales and is alleged to have engaged in a price war with Quidsi.131See id. Khan argues that when Amazon purchased Quidsi in 2010—allegedly under duress, given the price war—that Amazon eliminated competition and signaled other potential rivals not to repeat Quidsi’s mistake.132See id. at 671–72, 769–70. Khan highlights that, after the acquisition, Amazon ended some promotional offers, effectively raising prices to consumers.133Id. at 770–71. However, this assertion clashes with data available for retail online prices for six leading diaper brands, which fell in real terms by 18.25% between July 2010 (prior to Amazon’s acquisition of Diapers.com) and April 2019.134The brands included: Pampers, Huggies, Luvs, Seventh Generation, and Earth’s Best. Disposable Diapers Add Up! Unit Price of Popular Brands, Popsugar (July 15, 2010), https://perma.cc/JD4H-8WEU (providing diaper prices in 2010). The retailers listing April 14, 2019 online products were Target, Walmart, and Boxed.com (no 2010 Amazon prices were found for these retailers). 2010 prices were adjusted by the CPI.

The actual message transmitted to potential entrants is far different than what Khan supposes. In fact, Diapers.com entered the market for baby products easily, assisted by the availability of the Amazon sales platform. By 2010 it did, indeed, have the largest sales in its product line.135E.g., Erick Schonfeld, Diapers.com on Its Way To Selling Half a Billion Diapers, Raises $20 Million Debt Round, TechCrunch (Apr. 20, 2010, 7:11 AM), https://perma.cc/2QCQ-J7YU (“[T]he CEO of Diapers.com thought that they sold four times more diapers than the next largest seller.”). It was then the subject of a bidding war between Amazon and Walmart; its buyout by Amazon at $545 million reflected capital gains of about $400 million, and brought the Diapers.com entrepreneurs to work for Amazon—an outcome they highly prized.136Stone, supra note 79, at 296, 299. The merger was approved by the Federal Trade Commission because there existed a “plethora of other companies, like Costco and Target, that sold diapers both online and offline.”137Id. at 299.

Khan ends the story implying that Amazon had dealt competitors a painful blow. They had not. In 2013, Lore and Bharara, the now wealthy start-up veterans, left Amazon.138Greg Bensinger, Amazon’s Diapers.com Founders Jump Ship, Wall St. J. (July 8, 2013, 3:09 PM), https://perma.cc/PFE9-HFU4. Working together at Amazon, conflicts developed between Bezos and the Quidsi founders. Sharon Edelson, Marc Lore, Who Engineered Walmart’s Digital Transformation, to Step Down, Forbes (Jan. 15, 2021, 5:49 PM), https://perma.cc/WXN2-PH79. Soon thereafter, Lore founded a new online retail platform, Jet.com, that competed frontally, across hundreds of product lines, with Amazon.139Sarah Perez, Quidsi Co-Founder Raises an Additional $20M for His New E-Commerce Biz, TechCrunch (Sept. 16, 2014, 12:02 PM), https://perma.cc/NF8V-S29E. Lore was not intimidated, and his predatory scars were evidently not debilitating. Jet.com was then sold in 2016 for $3.3 billion—to Walmart.140Walmart Agrees to Acquire Jet.com, One of the Fastest Growing e-Commerce Companies in the U.S., Walmart (Aug. 8, 2016), https://perma.cc/PX6F-L73T. Until January of 2021, Lore, the vanquished Diapers.com start-up entrepreneur, headed the e-commerce operations of Walmart.com.141Matthew Boyle & Bloomberg, Walmart Head of E-Commerce Marc Lore Leaving Amid the Retailer’s Showdown with Amazon, Fortune (Jan. 15, 2021, 12:37 PM), https://perma.cc/HXW2-A7TQ.

D. Pillow Pets

A similar story is told about Pillow Pets, maker of a popular sleeping cushion featuring cartoon characters and sports logos. The products were sold on Amazon in 2011. Khan, uses a 2012 news story142Greg Bensinger, Competing with Amazon on Amazon, Wall St. J. (June 27, 2012, 6:15 PM), https://perma.cc/3NC4-XMJ5. to source her description of a predatory campaign waged by Amazon against an online retailer, Collectible Supplies Inc. (“Collectible”), a Southern California company that sold Pillow Pets “modeled after NFL mascots.”143Id. Much like Diapers.com, but without the buy-out, Amazon was alleged to have undercut the upstart rival, selling the NFL logo pillows for the same price but giving Amazon’s products “featured placement” on the site.144Id. The purpose, according to Khan, was for Amazon to take Collectible’s business for itself.145See Khan, supra note 17, at 781–82.

Collectible is still in business, and it is difficult—either through Khan’s description or her source, let alone financial records for a small, private business—to know what impact was felt by this company.146See Learn about Collectible Supplies, Collectible Supplies, https://perma.cc/MN5K-MZVP. What is clear, however, is that the creator of the Pillow Pets—Jennifer Telfer—used Amazon as a distributor, directly (by using Amazon as a retail platform) and indirectly (through intermediaries like Collectible who also sold on Amazon’s site). Jennifer Telfer is feted as one of America’s most successful female entrepreneurs, “produc[ing] millions of Pillow Pets annually.”147Joyce A. Glazer, Celebrating Women: Jennifer Telfer, San Diego Mag. (Jan. 31, 2017), https://perma.cc/24DM-FDJ2. In 2012, even as she was reported to be battling anticompetitive conduct in the online retail space, CNBC listed Telfer as owner of one of the “10 Ideas that Made $100 Million.”148Michelle Fox, 10 Ideas that Made $100 Million, CNBC.com (June 20, 2012, 9:38 AM), https://perma.cc/FPV4-PFUG. Her website currently lists her as CEO of Pillow Pets and notes that the company has sold 70 million “pets” worldwide.149“Jennifer Telfer, Founder and Chief Creative Officer of Pillow Pets®, is doing what most kids dream about doing . . . . [In 2003], Jennifer and her husband Clint started the Pillow Pets company . . . and today Pillow Pets are a household name . . . . Jennifer has designed and created thousands of versions of Pillow Pets selling over 100 million products worldwide . . . . Jennifer is honored to own a company whose products touch people’s lives in positive ways.” About the Creator, Pillowpets.com, https://perma.cc/XZK2-K9VQ. Telfer and her husband are reported to have started the company “with only $800 from their savings.” Ketty Law, Who Invented the Pillow Pet. The Story Behind It, Krostrade (Dec. 21, 2020), https://perma.cc/TES6-9LAN.

That Khan and the New Brandeisians select these stories to illustrate the problem of exclusion casts doubt on their argument. Rather, independent sellers are flocking to vertically integrated websites, including Amazon. Thus, Demsetz’s approach, asking how market structures are created and why they operate as they do, would seem the correct approach. When Khan asserts that “conflicts of interest that arise from Amazon both competing with merchants and delivering their wares pose a hazard to competition,”150Khan, supra note 17, at 780. marketplace experiences offer a cross-check. “The thousands of retailers and independent businesses that must ride Amazon’s rails to reach market are increasingly dependent on their biggest competitor,”151Id. but their revealed preference—driven by self-interest and informed by the dispersed, decentralized knowledge known to actual businesses—brings light upon the market process.

Conclusion

In perhaps the most sophisticated modern challenge to the Schumpeter-Demsetz view of markets, Eric Posner and Glen Weyl’s Radical Markets lays out the case for tectonic shifts in property rights to support new and improved social progress.152See generally Eric A. Posner & E. Glen Weyl, Radical Markets: Uprooting Capitalism and Democracy for a Just Society (2018). Their view is that stunning advances in efficiency brought forward by the “Gig Economy” expose not the productivity of creative destruction but the infirmities of existing concepts and law.153See id. at 26–28. “Markets are clogged with market power,” they write, and “[e]ven for many markets for relatively homogeneous commodities, such as Internet services or airplane flights, a few dominant firms prevail.”154Id. at 26–27. “We claim that market power is omnipresent and intrinsic to the current institutional structure of capitalism . . . .”155Id. at 27.

The authors do create a compendium of market imperfections, but that is child’s play. Their ideal is not the real. And the conclusion they offer travels a straight line that skips the relevant choices. Indeed, the grass is always greener. The markets condemned may possibly be improved with smart regime reforms, but the experimental evidence gathered suggests that inequality and conflict might also be far worse with such reforms.

For example, regulated airlines were cartelized under the Civil Aeronautics Board (“CAB”) rate setting, and consumer welfare suffered.156See, e.g., Dennis W. Carlton & Randal C. Picker, Antitrust and Regulation, in Economic Regulation and Its Reform: What Have We Learned 25, 50–52 (Nancy L. Rose ed., 2014); Hayden Rosenthal, A Tale of Two Industries: The Evolution of American Commercial Air Travel from Regulation to the Free Market, Aviation in Am., https://perma.cc/ALF4-EEYZ (noting the CAB’s disenfranchisement of smaller carriers and the active entry barriers and price manipulation that the agency would support). Air traffic passengers gained about a $20 billion annual premium following the abolition of that regime in 1985,157Alfred Kahn, Lessons from Deregulation: Telecommunications and Airlines After the Crunch (2003), 3. and that was the gentle news. In the initial fifteen years of the agency’s existence, regulators strongly favored first-class service and airfares. In one of the “most bizarre and illuminating chapters in the history of regulation,” Harvard law professor Louis Jaffe wrote in the 1954 Harvard Law Review, only 30% of air traffic could be sold at coach fares—and that discounting existed only because “unscheduled” airlines brazenly evaded a government ban.158Louis L. Jaffe, The Effective Limits of the Administrative Process: A Reevaluation, 67 Harv. L. Rev. 1105, 1111 (1954). “The CAB is completely committed to the existing certificated carriers,” Jaffe explained.159Id.; see also Thomas W. Hazlett, The New Trustbusters Are Coming for Big Tech, Reason.com (Oct. 2019), https://perma.cc/F8CF-Z9UN.

Ending the Interstate Commerce Commission in 1995 brought nearly twice the gains,160Hazlett, supra note 159 (referring to a Brookings Institution study that “pegged the efficiencies at $18 billion in 1996 alone”). and incidentally delivered substantial environmental improvements, such as in sulfur dioxide emissions.161Richard Schmalensee & Robert N. Stavins, The SO2 Allowance Trading System: The Ironic History of a Grand Policy Experiment, 27 J. Econ. Persps. 103, 103–04 (2013). Paring back common carrier regulations, stifling modern broadband deployments, was likewise key to discovering the possibilities of the commercial internet.162See Thomas W. Hazlett & Anil Caliskan, Natural Experiments in U.S. Broadband Regulation, 7 Rev. Network Econ. 460 (2008); Jason Oxman, The FCC and the Unregulation of the Internet (Fed. Commc’ns Comm’n Off. Plans & Pol’y, Working Paper No. 31, 1999), https://perma.cc/7Q6N-LT6X. See also Peter Huber, Law and Disorder in Cyberspace: Abolish the FCC and Let Common Law Rule the Telecosm (1997). As was liberalization of radio spectrum property rights key to unleashing mass market mobile connectivity, the wireless web, and app stores that offer millions of software programs.163See Thomas Winslow Hazlett, The Political Spectrum: The Tumultuous Liberation of Wireless Technologies, from Herbert Hoover to the Smartphone (2017). These episodes inform history and our current institutional choices. There is no perfect competition. The relevant options are among pathways that, at best, skirt Nirvana.

But utopian vision takes some all the way to the Socialist Calculation Controversy. In an ambitious prediction, Posner & Weyl raise a flag to be planted on a future space mission.

In response to Hayek, Lange said “Let us put the simultaneous equations (governing the market) on an electronic computer and we shall obtain the solution in less than a second.” The seed of truth in this claim had been identified just six months before Lange’s death in 1965 by technology entrepreneur Gordon Moore.

Moore observed that the density of microchips and the computing power that could be achieved for a given cost doubled roughly every eighteen months. While this “Moore’s Law” was a wild extrapolation rather than a well-founded principle, it has largely held up. Because of this rapid development of computational capacity, the dream of a computer network that can achieve the complexity of the human mind is no longer out of reach. Most engineers believe that in the near future, probably the 2050s, the total capacity of digital computers will exceed that of all human minds.

When this point has been reached, the computational critique aimed at Lange will no longer hold. In principle, the market could be replicated in silicon—replacing the distributed, parallel flesh-and-blood system that we are familiar with. . . . The technological problem in aggregating information can be solved.164Posner & Weyl, supra note 152, at 286–87.

This modern argument adds to Demsetz’s litany; the “Big Data Fallacy” may one day take its rightful place next to Nirvana, Free Lunch, and Greener Grass. In radio spectrum allocations, the “end of scarcity” argument experienced a bubble in the early 2000s, as advanced computational techniques were said to eliminate conflicts in frequency use.165E.g., Gregory Staple & Kevin Werbach, The End of Spectrum Scarcity, IEEE Spectrum (Mar. 1, 2004, 15:16 GMT), https://perma.cc/EY33-NZ59. Since that time, throughput in wireless communications have increased about 128-fold, using the standard estimate provided by Cooper’s Law (for a given cost, wireless data traffic doubles every thirty months, a rough relationship observed for about the past century).166Martin Cooper, Internet: A Life-Changing Experience, IEEE Multimedia, April–June 2001, at 11–15; see also Cooper’s Law Acting on Media, Digital Deliverance, https://perma.cc/YFH2-GUAV. Alas, scarcity still reigns, as seen in the ongoing rent seeking for rival frequency allocations, and in the bidding for access to airwaves opening new opportunities in 4G, 5G, satellites, and a host of wireless applications beyond.167See, e.g., Bevin Fletcher, FCC Sets October Start Date for 3.45 GHz Auction, Fierce Wireless (June 9, 2021, 5:52 PM), https://perma.cc/YHT4-D7EJ (noting the beginning of a spectrum auction for a frequency that is part of a larger spectrum demand “viewed as a key for 5G services”). . In government auctions and secondary markets, competition to obtain property rights in airwave spaces survives technological upgrades.

The view that science conquers scarcity exudes “asymmetric triumphalism,” portraying the supply side of progress—say, advances in information processing—while ignoring the simultaneous demand-side impacts unleashed by the wider options that these discoveries trigger. Innovations that improve old ways of doing business (or policy) allow human action to operate under looser constraints, but simultaneously drive new contests. New social coordination challenges continue to drive demand for property rights, evolving in structure and ever-adapting.168See Demsetz, Toward a Theory of Property Rights, supra note 3. The Demsetz approach of realistic institutional comparisons offers a guidepost in this endeavor, future-proofing our theory of markets in the bargain.

How rules can best guide this momentum towards human progress remains a choice between possible outcomes. Nirvana is not one of them. Not today, not when Demsetz called attention to this Fallacy a half-century ago, and probably not in the 2050s. I will gladly put money on my assertion. Should Nirvana arrive, I will be delighted to pay the bet.